Trends

US smartphone shipments plummet 19% YoY as upgrades slow

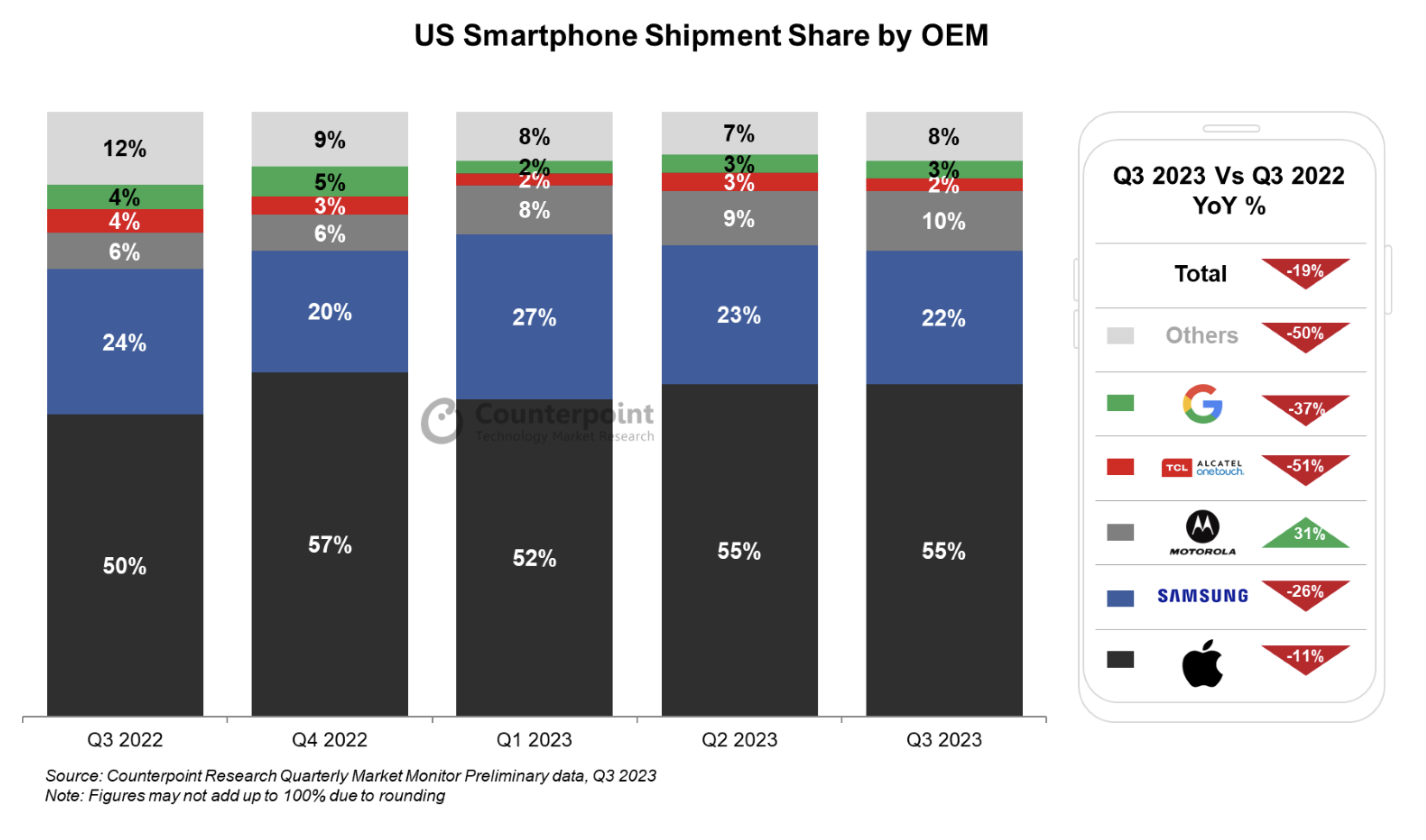

US smartphone shipments declined 19% in Q3 2023, according to Counterpoint Research’s Market Monitor data. Samsung, Google, and TCL saw steep declines of 26%, 37% and 51%, respectively, in their smartphone shipments. However, Motorola and Nokia HMD managed to increase their shipments by 31% and 17%, respectively, compared to the same period last year. Apple’s shipments were down 11% compared to Q3 2022, part of which is attributable to the later launch date of the iPhone 15 series compared to the iPhone 14 series, which pushed some shipments into Q4 2023.

Commenting on the Q3 2023 performance, Research Analyst Matthew Orf said, “OEMs were cautious to increase their shipments during the quarter as consumer demand remained low. While upgrade rates were slightly up at the carriers when compared to last quarter, they remained much below their usual levels as consumers opted to hold on to their devices for longer instead of upgrading. Improved durability with stronger build quality, less impressive upgrades among new smartphone releases, and an uncertain macroeconomic environment have all contributed to the malaise we are seeing in the US smartphone market.”

Senior Research Analyst Maurice Klaehne said, “Despite the 19% decline in overall smartphone shipments, there were some brands that saw growth. Motorola and Nokia HMD were able to buck the market trend and achieve growth with refreshed portfolios and stronger presence in prepaid and national retail channels. Samsung and TCL struggled in the low end of the market with devices approaching their end of life (EOL).”

On foldables market trend, Klaehne said, “Foldables are one potential bright spot in the US smartphone market, with increasing number of Android foldables options. Samsung launched its Galaxy Z Flip and Fold 5 in August, while OnePlus launched its first foldable and Motorola launched the sub-$900 Motorola Raz 2023 in early Q4 2023.”

Commenting on the prepaid and postpaid market landscape, Associate Director Hanish Bhatia said, “Postpaid carriers continue to face strong competition from cable players Spectrum and Xfinity. This is driven by aggressive promotions and bundling of mobile with broadband. Verizon has been on the back foot but scaling its 5G mid-band coverage quickly in 2023-24. On the prepaid side, H1 2023 saw a lot of action with T-Mobile’s acquisition of Mint Mobile, Verizon losing TracFone subscribers while expanding Total Wireless’ retail footprint, Dish consolidating its prepaid brand portfolio, and new MVNOs entering the retail landscape.”

Commenting on the iPhone 15 launch and overall market outlook, Research Director Jeff Fieldhack said, “Despite the carriers continuing to offer strong promotions through the quarter, upgrade rates at the carriers remained near record lows. We expect a seasonal rebound in upgrade rates during the fourth quarter, but they are likely to remain lower than in the same period last year. There is a large installed base of iPhone 11 and iPhone 12 users in the US that is likely to upgrade to the iPhone 15 series this year. But while we saw the usual high wait times for the iPhone 15 series at launch, they came back down to earth quicker than for the iPhone 14 series, which could signal that the slump in consumer smartphone demand will extend to the iPhone 15 in Q4 2023.” Counterpoint Research

You must be logged in to post a comment Login