Headlines of the Day

Vodafone Idea: Running to stand still

Vodafone Idea (VI), has, once again, taken a corporate decision, which for all practical purposes, will help it run to stand still. This month, the VI board approved of a government option (aid) -– to convert the full amount of interest on spectrum auction and AGR (adjusted gross revenue) dues, which it owes to the government, into equity.

With this move, the government will soon become VI’s largest shareholder with a 35.8 percent stake, followed by UK’s Vodafone Group holding a lower 28.5 percent stake (44.39 percent earlier) and Aditya Birla Group 17.8 percent (27.66 percent earlier). The process is expected to be completed in a few months, the company said. This essentially implies that a potential investor may end up getting a lower stake -– unless the government sells its stake — and have to invest more into VI. Unless VI can continue to raise its product prices, increase its average revenue per unit (ARPU) and turn profitable.

Vodafone Idea has reported nine successive quarterly losses, including a quarterly loss of Rs 7,132.3 crore for the three months to September 2021 on a 2.8 percent rise in revenues from the previous quarter to Rs 9,410 crore.

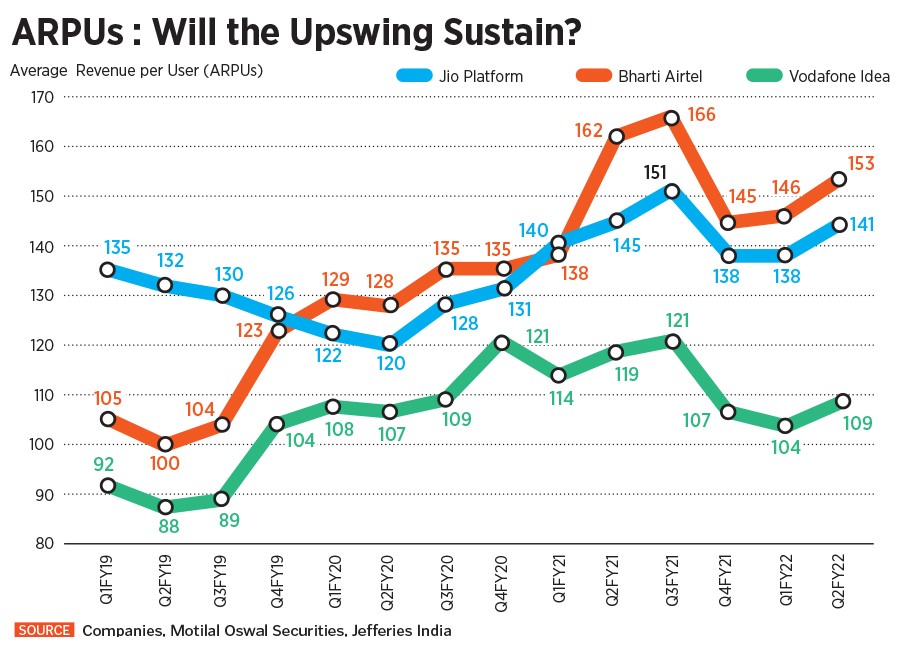

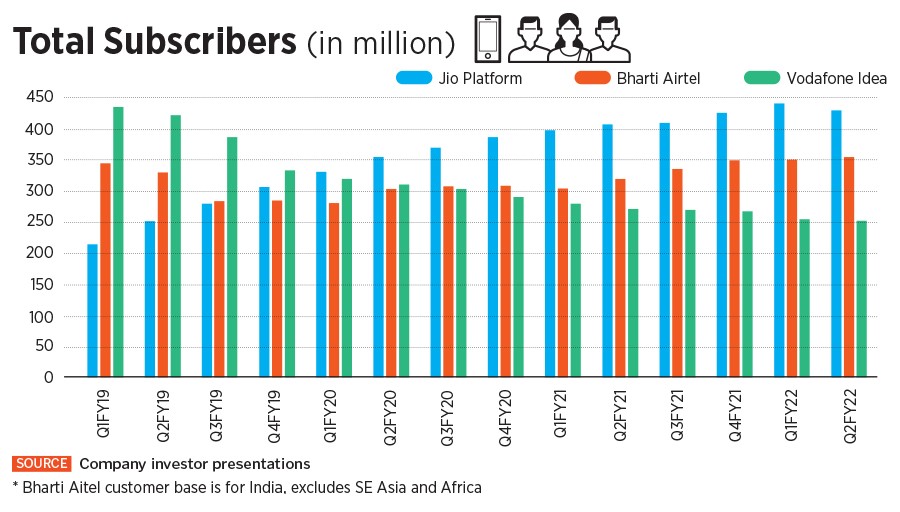

Once the fastest-growing telecom company, VI has continued to lose subscribers and market share to leader Reliance’s Jio Platforms and rival Bharti Airtel over the past three years (see charts). VI is scouting for fresh capital which would help the company lower its gross debt of Rs 1.94 lakh crore, as of September-end quarter. It also needs to invest in the upcoming 5G technology network expansion and compete with Jio and Airtel, while also trying to arrest its falling market share.

Is VI more attractive?

Though the government is not expected or likely to run VI’s daily operations, does this move to opt for equity conversion make VI any more attractive to new investors or efficient as a company? “The jury is out on this one,” says former Bharti Airtel CEO Sanjay Kapoor, who is now an entrepreneur and TMT consultant advising various telecom companies. Bharti Airtel, which had been offered a similar option of conversion of debt to equity, has declined to take it.

The government’s option to convert debt owed to it into equity does not help it or Vodafone Idea. VI was anyway not expecting to pay up this amount for at least four years, so it only appears to be a book transaction. And, any government would prefer to get its debt back and not hold on to equity, but the onus to sell it falls on the government. So the equity conversion was “neither what the government ideally desired nor possibly Vodafone Idea’s first choice. It is a marriage of convenience under the trying circumstances,” Kapoor says.

For months now VI’s CEO Ravinder Takkar has told media that international investors have been keen to pump in money into India’s telecom sector and it was in active discussion with potential investors. “This [equity conversion} is positive for the fund raise. I hope to be back shortly to announce the fund-raise process,” VI’s CEO Ravinder Takkar told media a day after the board’s move on equity conversion.

No one doubts VI’s ability to either be able to borrow more from banks or even find a new investor, but it needs to be a substantial amount of money. The reality is that VI is now a distant third player behind Jio and Bharti Airtel. Jio has a 35. 7 percent market share in the total active wireless subscriber base, followed by Airtel with 34.8 percent and Vodafone 23.7 percent. So, why would an investor put in money when questions are still being raised over its survival and competitiveness? Vodafone is in a silent period ahead of its December quarter ended earnings, so declined to comment on forward looking issues.

The net present value (NPV) of this interest is expected to be about Rs 16,000 crore as per VI’s own estimates, subject to confirmation by the Department of Telecom. Since the average price of the company’s shares at the relevant date of August 14 last year was below par value, the equity shares will be issued to the government at par value of Rs 10 per share.

The role of the existing promoters of VI in coming months will be integral to how the company fares. Takker has clearly said that “the existing promoters are fully committed to running the operations of VI and that the government does not want to be involved in this role or have a nominee on the VI board”.

One must not forget here that billionaire industrialist Kumar Mangalam Birla, who heads the Aditya Birla Group, had in August 2021 expressed his willingness to offer his, then 27.6 percent, promoter stake to the government or any other domestic entity that the government may consider worthy, to keep the company alive. This was just prior to the ‘rescue package’ that the government came out with for telecom operators. VI and Bharti Airtel took advantage of a lifeline from the government by accepting a four-year moratorium for them to pay up statutory dues. What Birla would be tempted to do now is anybody’s guess.

More tariff hikes needed, solo

The only way Vodafone Idea might depend less on what its promoters may or may not do is by strengthening its financials. And this would only come by boosting its income by raising tariff for its voice and data packages. VI did it twice in 2021 for some of its entry-level prepaid packages and some postpaid ones, but it was after Airtel’s moves a few days earlier in November. Now VI will need to do it on its own. And more often.

This would be beneficial for Jio and Airtel too as ARPUs move north for the sector. But with it comes the risk of a higher churn of subscribers. A churn in the telecom sector means the percentage of subscribers moving from a specific service or a service provider to another in a given period of time. Analysts expect VI to continue to see a churn in the near term.

“Even 3QFY22 (December-ended quarter) is expected to see a nearly 4 to 5 million subscriber churn. Until VIL has sufficient funds to invest in the network and compete in the market, the subscriber churn may continue to dilute earnings,” Motilal Oswal’s telecom analyst Aliasgar Shakir says.VI had seen a lower churn of 2.9 percent in the September-ended quarter, against 3.5 percent in the sequential quarter earlier.

“VI would need hike tariffs –- leading to an ARPU increase of around 1.9x — to reach a self-sustainable level over the next four years. Alternatively, it may need to grow its revenue around 3x from current levels,” Shakir adds in a note to clients.

VI’s current ARPUs are at Rs 109 (28 percent lower than leader Airtel’s Rs 153). Even taking an annualised figure of Rs 124 for VI’s ARPUs by March 2022 end, Motilal Oswal Securities’ analysts say its ARPUs will need to rise by 188 percent to Rs 357. Jayesh Bhanushali, AVP (Research), with IIFL Securities said that ARPUs have to double to Rs 207 by March-end FY24 from the current Rs 109 levels. “We look at the ARPU increase required to bring down VI’s net debt to Ebitda to 10x by end-FY24,” Bhanushali says.

The government holding such a large stake in VI is “their initiative to save the telecom industry from turning into a duopoly,” Bhanushali says. In the short-term the VI stock may react negatively due to the equity dilution at such a low price, but eventually as ARPUs rise –- as the trend has been in the last few quarters -– he expects the company to perform better in the long term. The VI stock has risen 46 percent since mid-July 2021 to Rs 12.9 on January 14 at the BSE, but has been down nearly 17 percent in the New Year, after digesting the equity conversion move.

Judicious spending

Assuming additional funding for VI comes at some stage the tricky part will be how VI allocates this funding across existing telecom circles. Will it put good money after bad? VI has 17 priority circles, and claims to be a market leader in two circles, Kerala (41 percent) and Mumbai (29 percent) based on revenue market share, as of September ended VI’s own data. It was a leader in Gujarat till June 2020. Similarly, in the states of Haryana, Maharashtra, Kolkata and Madhya Pradesh, it was the number 2 operator according to June 2020 data, but here it has now slid to the number 3 position. It will surely have to only invest in the circles where it stands a chance to make more money.

Vodafone has its attention on upgradation to 4G and enhancing customer experience. Over the medium term, the company is transitioning towards a technology-focussed company from a telecom operator, by working with partners to provide a range of multi-cloud services.

While the battle for VI, with or without funding, is going to be stiff, the one positive is that the government is trying its best to ensure that a duopoly does not get created in the telecom space. Oligopoly in telecom is a settled structure in countries which have higher ARPUs such as Canada, Australia, France and Germany. The third player lags behind but survives well. But in low ARPU nations such as India, Uganda, Sri Lanka, Bangladesh, the balance sheets of the third player will get stretched due to higher costs. In those terms, the chances of VI surviving into the short- and medium term are high, but as a distant third player.

For the dynamics to change further, it needs more help from the government. “The government will need to look at the industry very differently. They know that they need to create a virtual infrastructure which competes globally. Therefore they will have to view it as an infrastructure industry, meant to run the economy and treat every policy accordingly like how China and UAE do,” Kapoor says. That, alongside a liquidity and financial boost, will be a huge positive for the telecom sector.

VI hopes to finalise some funding by March-end 2022. The focus then will quickly shift towards 5G auctions, which are expected to take place in a few months’ time, after the regulator submits its recommendations to the Department of Communications. VI will, like Airtel and Jio, hope for lower pricing and better payment options while investing towards 5G technology. So, once again, it’s going to be another few crucial quarters for VI. Forbes India

You must be logged in to post a comment Login