Towers

Tower Signals

The telecom towers industry in India is in the process of a structural overhaul. Change in the base transceiver station (BTS) technology mix (2G/3G to 4G), consolidation in the industry, and gradual exit of smaller tower operators have changed the landscape.

The telecom towers industry in India is in the process of a structural overhaul. Change in the base transceiver station (BTS) technology mix (2G/3G to 4G), consolidation in the industry, and gradual exit of smaller tower operators have changed the landscape.

The Indus Towers-Bharti Infratel merger, expected to be completed by late 2019, is set to create the world’s second largest mobile tower operator, with over 163,000 towers and 36% tower market share in India. Post-merger, the industry will have three large players controlling over 70 percent tower market share. The balance will be shared among smaller towercos and telcos having captive towers.

Meanwhile, the telecom industry is also in the midst of structural changes. The consolidation wave has reduced the number of players to about five as of 2019, from ~15 players in 2012. With telecom operators divesting in tower assets, the towers industry is expected to the shift to pure-play independent towercos from the operator-led model.

Towercos hit hard by tenancy losses

Consolidation in the telecom industry has changed the dynamics of towercos. The latter reported massive tenancy losses over the past one and half years. For instance, the recent merger of Vodafone and Idea has resulted in over 57,000 tenancy losses. Further reduction of ~21,000 tenancies is expected in the first half of fiscal 2020. While exit penalties are expected to partially offset the revenue loss, the impact of tenancy losses is expected to spill over to fiscal 2020 as well.

The telecom sector moving towards an oligopolistic structure, with three players accounting for more than 90% market share, will pose challenges for towercos. This will put pressure on rent revenue per tower as the number of tenants per tower would go down. Further, the stressed financial condition of debt-laden telecom incumbents will restrain any material hike in rentals, at least over the medium term. In addition, through the towers added by Bharat Sanchar Nigam Ltd and Reliance Jio account for a considerable share of captive towers, the revenue from these towers does not flow to the industry.

The telecom sector moving towards an oligopolistic structure, with three players accounting for more than 90% market share, will pose challenges for towercos. This will put pressure on rent revenue per tower as the number of tenants per tower would go down. Further, the stressed financial condition of debt-laden telecom incumbents will restrain any material hike in rentals, at least over the medium term. In addition, through the towers added by Bharat Sanchar Nigam Ltd and Reliance Jio account for a considerable share of captive towers, the revenue from these towers does not flow to the industry.

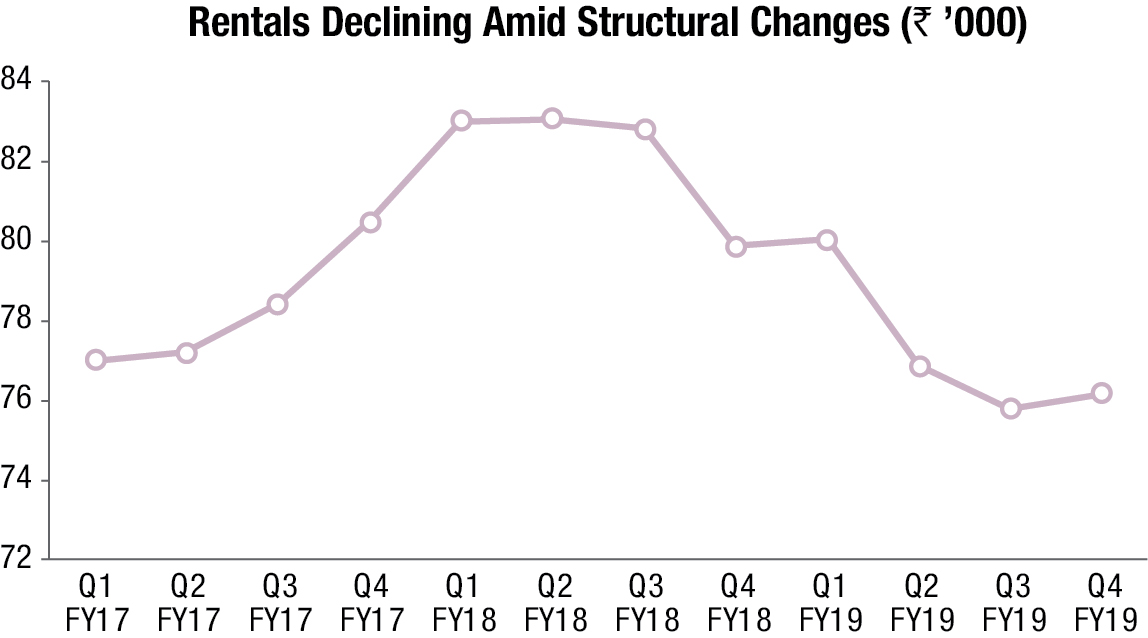

A look at tower rentals in the past 12 quarters indicate a stabilising trend in till the first half of fiscal 2018 and then a drop for the first time in 5 years in the second half of fiscal 2018 owing to tenancy losses.

A look at tower rentals in the past 12 quarters indicate a stabilising trend in till the first half of fiscal 2018 and then a drop for the first time in 5 years in the second half of fiscal 2018 owing to tenancy losses.

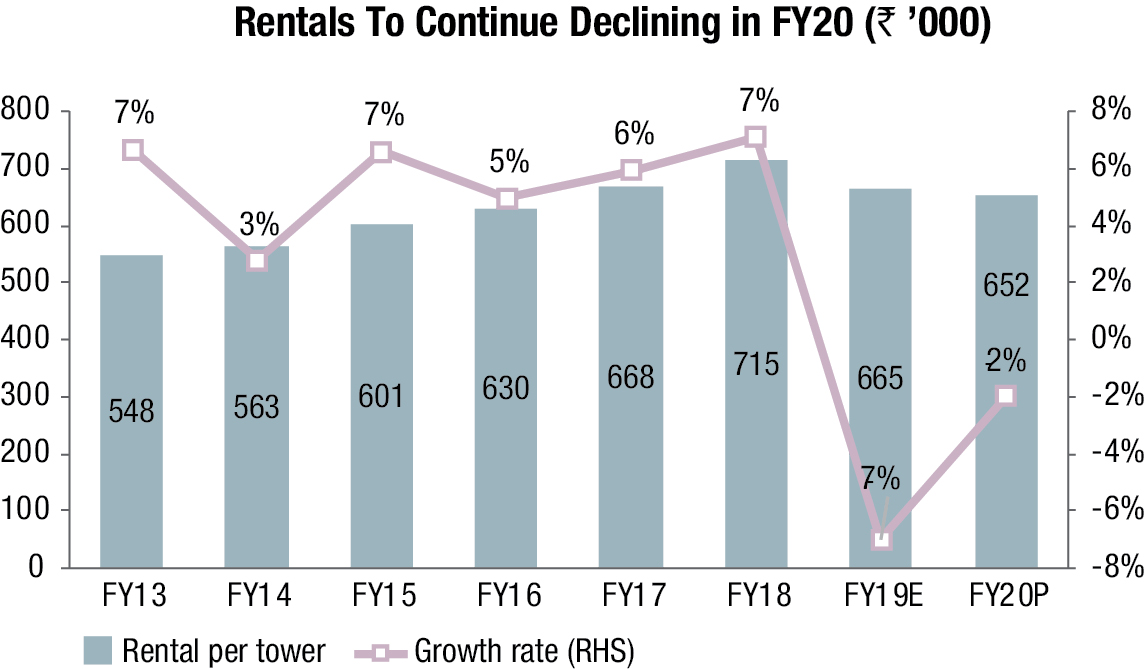

Our industry interactions suggest that telcos are currently focusing on densification of 4G networks. The replacement of 2G and 3G BTSs with 4G ones will slow down net BTS additions to ~1.55 lakh in fiscal 2020, against ~2.75 lakh in fiscal 2019. The number of BTSs per tower is, however, expected to increase marginally to ~3.85 this fiscal, compared with ~3.67 in fiscal 2019, on increased loading by telcos to increase their capacity per site and support existing coverage during high traffic and congestion. This loading results in a discount to telcos (need to pay just 1015% of rent), which reduces the potential for higher topline of towercos.

Going forward, loaded sites are expected to account for a higher proportion of incremental tenancies. In addition, rentals might come under pressure during contract renewals as telcos have higher bargaining power. This is because telcos’ return on capital employed (RoCE) is less than ~2%, compared with towercos’ RoCE, which is as high as 1920%. Post a decline of ~7% in fiscal 2019, CRISIL Research expects the rent revenue per tower to remain under pressure and decline by another 2-3% in fiscal 2020.

Telcos betting to correct debt profile

Telecom sector debt remains elevated due to high network investments and spectrum price. CRISIL Research estimates the total debt to be ~Rs 4.3 trillion as of March 2019. Meanwhile, the continued deterioration in price realisation has led to weak cash accrual. Thus, telcos are resorting to measures such as selling standalone towers or reducing stake in existing tower subsidiaries, to pare debt.

For instance, Vodafone and Idea, last year, sold ~20,000 standalone towers to American Tower Company (ATC) at ~Rs 78 billion. Bharti Airtel has raised over ~Rs 120 billion through multiple rounds of stake sale in Bharti Infratel. Recently, ATC has acquired ~13 percent residual stake of Tata Teleservices in ATC Telecom Infrastructure at ~Rs 25 billion.

Bharti Airtel and Vodafone Group both are in talks to slash their stakes in the Bharti Infratel and Indus Towers merged entity. Post-merger, Vodafone Idea has an option to sell its 11.15 percent stake in Indus, which has an implied value of ~Rs 62 billion for cash at completion.

The sale of assets coupled with the recent rights issue of ~Rs 500 billion by various players is likely to reduce the debt of telcos in fiscal 2020, but valuations of tower assets will remain a key monitorable.

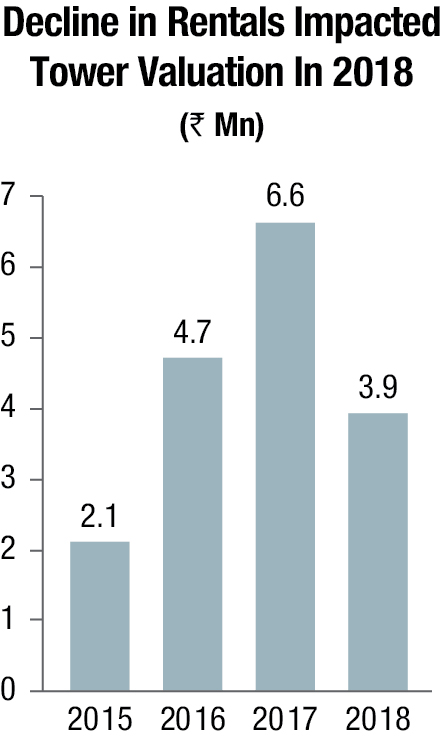

Tower valuations declined; future valuations a key monitorable

The valuation of tower portfolios depends on factors such as geographical presence, clientele, and master service agreements. ATC has been acquiring the tower portfolios of small players in India. ATC’s Viom acquisition in 2015 made it a leading independent telecom infrastructure provider and helped it to compete with other big players such as Bharti Infratel and Indus Towers and acquire ~16 percent of tower market share as of fiscal 2019 from ~2 percent as of fiscal 2012.

The valuation of telecom towers is based on defined cash flows to towercos backed by long-term contracts with telcos. Typically, large telcos have 8-10 years of contract period with towercos.

Between 2015 and 2017, tower rentals grew at 5-7 percent on-year, with tower valuations rising in tandem. However, the decline in rentals in 2018 seems to have impacted the valuation of towers, as is evident from the chart below. CRISIL Research believes the valuations to stay subdued in the near term, as rentals are unlikely to go up. Besides, increased investment in newer technologies like small cells, in-building solutions, massive multiple-input and multipleoutput or MIMO and Wi-Fi hotspots might also keep tower valuations under check. – Crisil Research

You must be logged in to post a comment Login