Trends

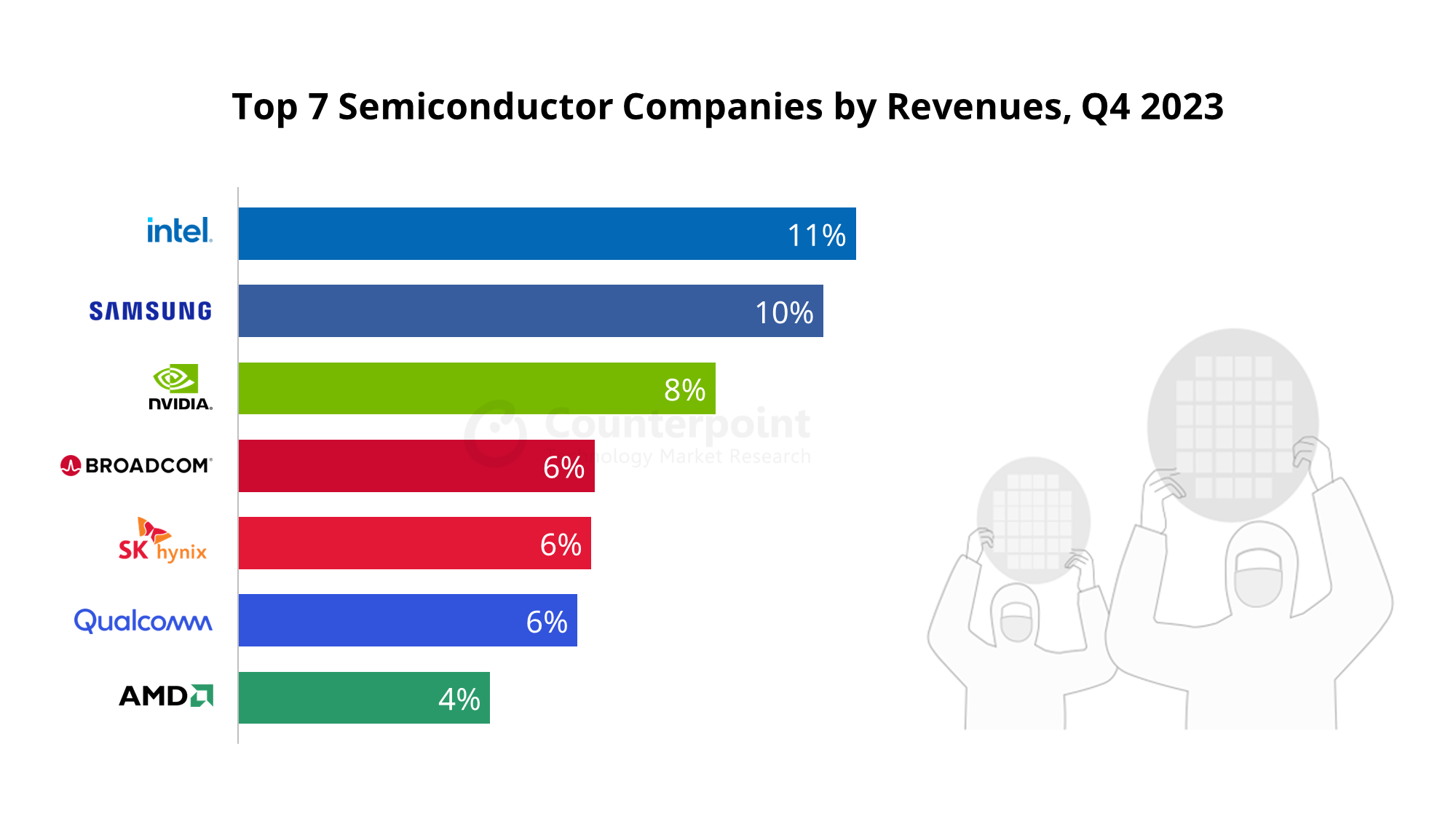

Revenue by top 7 semiconductor firms during Q4 2023

In Q4 2023, Intel claimed the top spot in the global semiconductor market mainly due to the normalizing client computing sector, which saw a 12% QoQ growth. Samsung ranked second with a flattish QoQ revenue largely driven by the memory revenue rebound but capped by the mobile business weakness. NVIDIA’s dominance in AI servers continued to support its semiconductor revenue growth and thus ranking the company #3 in Q4 2023. Broadcom claimed the fourth spot mainly due to a strong demand in AI data centers and AI accelerators from hyperscalers. SK hynix also benefited from memory recovery and reported a sequential revenue growth to rank #5 in the quarter. Qualcomm and AMD also reported sequential revenue growth and ranked #6 and #7.

Infographic: Foundry Companies’ Revenue Share in Q4 2023

Foundry Companies’ Share by Revenue

In Q4 2023, TSMC maintained its dominant position in the foundry sector, commanding a formidable 61% market share driven by smartphone restocking and strong demand from AI. Samsung Foundry retained its status as the second-largest player with a 14% market share, benefiting from smartphone restocking and positive initial pre-orders for the Samsung S24 series. GlobalFoundries and UMC both captured a 6% market share. However, subdued demand and customer inventory adjustments, particularly in automotive and industrial applications, impacted the 2024 guidance for both companies. SMIC held a 5% share and anticipates increased demand for smartphone-related components in the short term. Despite this, a cautious outlook prevails for the full year due to uncertainties in demand sustainability, echoing muted sentiments across mature node foundries.

Foundry Industry Share by Technology Node

In Q4 2023, the 5/4nm node captured the top position with a 26% market share driven by strong demand for AI applications. Following closely behind was the 7/6nm node, representing 13% of the market, fueled by low-mid-end smartphone restocking demand. The 3nm node, with a 9% market share, experienced growth driven by the ramp-up of the iPhone 15. Both the 28/22nm and 16/14/12nm nodes also held a 9% market share each. The former benefited from the resurgence in smartphone restocking, particularly for AMOLED DDIC components.

Infographic: Global Smartphone AP Market Share in Q4 2023

Global Smartphone AP Market Share by Shipments

MediaTek dominated the smartphone SoC market in Q4 2023 with a share of 36%. MediaTek had a strong fourth quarter with inventory restocking by smartphone OEMs. Growing demand for 5G and 4G SoCs and the successful ramp-up of the company’s third-generation flagship SoC, the Dimensity 9300, contributed to the growth. Qualcomm captured a 23% share in the smartphone AP/SoC market during the quarter. Qualcomm’s shipments increased in Q4 2023 due to restocking by smartphone OEMs and design wins for flagship chipsets Snapdragon 8 Gen 3 and Snapdragon 8 Gen 2 from Chinese smartphone OEMs.

Global Smartphone AP Market Share by Revenue

Apple dominated the AP market in Q4 2023 in terms of revenue with a 39% share. Apple’s revenue increased QoQ due to the launch of the iPhone 15 and iPhone 15 Pro series. Qualcomm captured the second position in the AP market in Q4 2023 with a 34% revenue share. The premium segment drove Qualcomm’s revenue with the launch of the new Snapdragon 8 Gen 3 chipset. Also, design wins for flagship chipset Snapdragon 8 Gen 2 from Chinese smartphone OEMs added to the revenues. MediaTek captured the third position with a share of 15% in the total global smartphone AP/SoC revenues. MediaTek’s revenue increased QoQ in Q4 2023 as the inventory restocking was done by smartphone OEMs. Counterpoint Research

You must be logged in to post a comment Login