Trends

Indonesia’s Q2 2022 smartphone shipments decline 11%

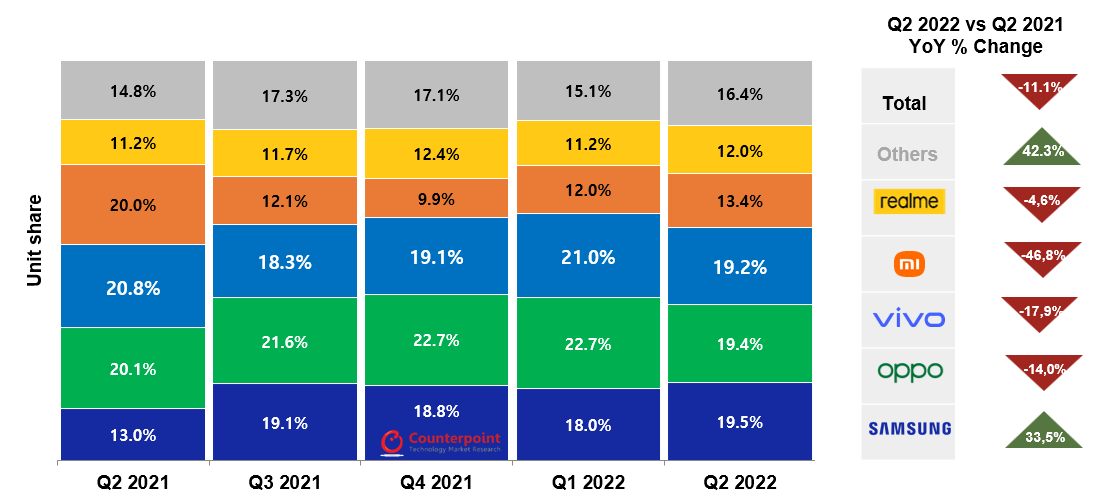

Indonesia’s Q2 2022 smartphone shipments fell 11% year-on-year to 9.4m units, according to Counterpoint’s latest Monthly Indonesia Smartphone Channel Share Tracker.

The disappointing results reflected broader regional and global trends where macro headwinds and currency issues made for a tough quarter. Base effects were also in play, as severe lockdown restrictions last year boosted demand for smartphones as more people spent more time online, magnifying the impact of this year’s economic woes.

Demand for budget devices (<$150), which account for a big portion of the market, fell the most, with shipments falling after Ramadhan and Eid Al Fitr. The latter half of the quarter was especially bad; June was off by almost 1m units compared to last year in the budget category.

Samsung was the only gainer in terms of unit shipments, which grew by a massive 33% – though much of it was due to base effects as the vendor struggled last year from supply issues stemming from its Vietnam factory shutdown.

Nevertheless, Samsung flooded the market by launching various low-to-mid end devices like it’s A and M series, which did especially well in April, accounting for 14% of total domestic shipments during the festive month. It was enough to help the company take pole position in terms of market share for the first time in three years, but not enough to match pre-COVID levels.

Xiaomi saw the biggest slide as chipset supply issues continued to plague shipments after its record Q2 2021. The latest quarter saw shipments fall YoY by an astonishing 47%.

![]()

More broadly, online channels ticked up as OEMs and major e-commerce sites offered promotions to help drive sales. Almost one out of every five smartphones shipped last quarter were through online channels. “What’s interesting to see is the fast rise of domestic fintech player Akulaku, which grabbed third spot last quarter in online shipments,” notes Senior Analyst Febriman Abdillah. “One of the ways they grabbed share was by providing buyers with Akulaku instalment plans. This ‘pay later’ pricing strategy will be important in growing the mid-end of the market, especially considering the current macro climate.”

Looking forward to 2H, our expectations for Indonesia remain tempered. Although it is less vulnerable to a recession than some of its regional and global peers, currency fluctuations will likely play a strong role in driving or hampering smartphone demand and our global macro outlook implies elevated inflation risk. Reduced spending power will hit segments shopping for low-to-mid end devices the hardest – making domestic smartphone demand especially vulnerable over the second half of 2022. However, there is room for some optimism as the upcoming 3G shutdown and continued digital transformation efforts will lead consumers to upgrade their phones.

“We’re expecting to see not only 3G replacement drive the lower end of the market, but consumers upgrading from 4G to 5G, which reached 1.96m units for Q2, to help boost higher-value segments as people look to enhance their online experience,” says Senior Analyst Glen Cardoza. “This is good news for the mid-end of the market, which today delivers some incredible value in terms of specs.”

“We are also keeping our eye on e-sports and smartphone gaming in the region. We expect specs to support this type of gaming to become mainstream across mid-end devices. Hence, beyond 5G, we see this as another upgrade driver, particularly amongst younger users – a massive demographic in Indonesia.”

CT Bureau

You must be logged in to post a comment Login