Trends

Indonesia smartphone market declines 12.4% YoY in 3Q21

According to the latest IDC Quarterly Mobile Phone Tracker, Indonesia’s smartphone shipment dropped 12.4% YoY, reaching only 9.2 million units in 3Q21 amidst channel disruptions and difficulties from the supply side. The second wave of COVID-19 peaked in July 2021, resulting in stricter lockdown regulations that lasted for a significant part of 3Q21. This, in turn, led to a retail shutdown that impacted the Java and Bali regions and several other hotspots, which caused offline sales to suffer.

While restrictions started to ease since September, supply shortages will continue to impact overall mobile phone production and shipments, with a tighter supply of 4G smartphones as OEMs focus on 5G smartphones. This, along with the increasing component prices, led to price increases for several low-end 4G models. “Vendors are being strategic in facing this difficult supply situation, with some vendors opting to replace or not release models that had more supply constraints,” says Vanessa Aurelia, Associate Market Analyst from IDC Indonesia. “Some vendors started to explore other ways such as revisiting their distribution strategies to keep prices under control,” Aurelia added.

More 5G models continued to be released in 3Q21, increasing the share of 5G to 7% from 6% in the previous quarter. The average selling price (ASP) of 5G smartphones dropped by 27% QoQ to US$ 418 in 3Q21, as OEMs strive to bring affordable 5G smartphones into the market.

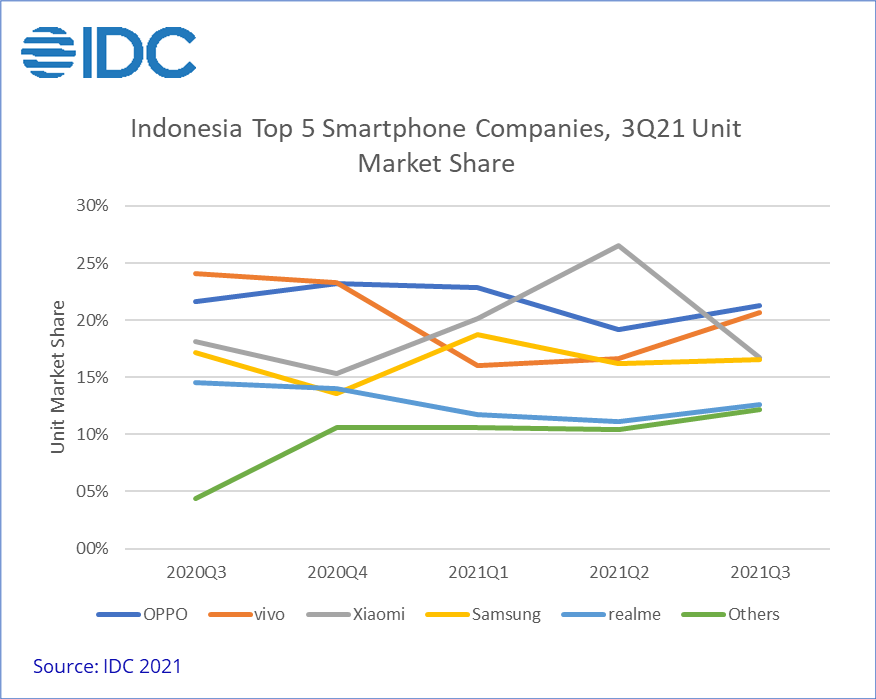

Top 5 company highlights 3Q21:

OPPO managed to climb back to the top position keeping a relatively steady inventory, despite the supply shortages. It was still the leader in the low-end segment (US$ 100 < US$ 200), which accounted for the majority of its shipments.

vivo managed to climb to the second position as it was able to grow its offline sales and maintain inventory level. vivo was able to enter the ultra low-end segment as the price of Y1s dropped to below US$ 100 while also taking second place in the low-end segment with its Y series.

Xiaomi dropped to the third position after two consecutive quarters of strong growth, as it faced supply constraints and tight inventory. Despite this, Xiaomi stood strong as the leader of the mid-range segment (US$ 200 < US$ 400).

Samsung kept its place in the fourth spot while experiencing shipment decline as lockdown-induced retail shutdown led to the slowdown in offline sales. Samsung also refreshed its foldable series in 3Q21, which were very well received by the market.

realme remained at the fifth position by maintaining its shipment number despite concerns of supply shortages. It was able to keep momentum by refreshing some of the C series models with a new processor that had a relatively stable supply.

OEMs are expected to be launching new models in tandem with the year-end holiday period in 4Q21 to utilize the momentum. However, the existing supply constraints are expected to persist weighing down on the overall shipment.

CT Bureau

You must be logged in to post a comment Login