5G

Hyperscalers eating into telcos’ margins

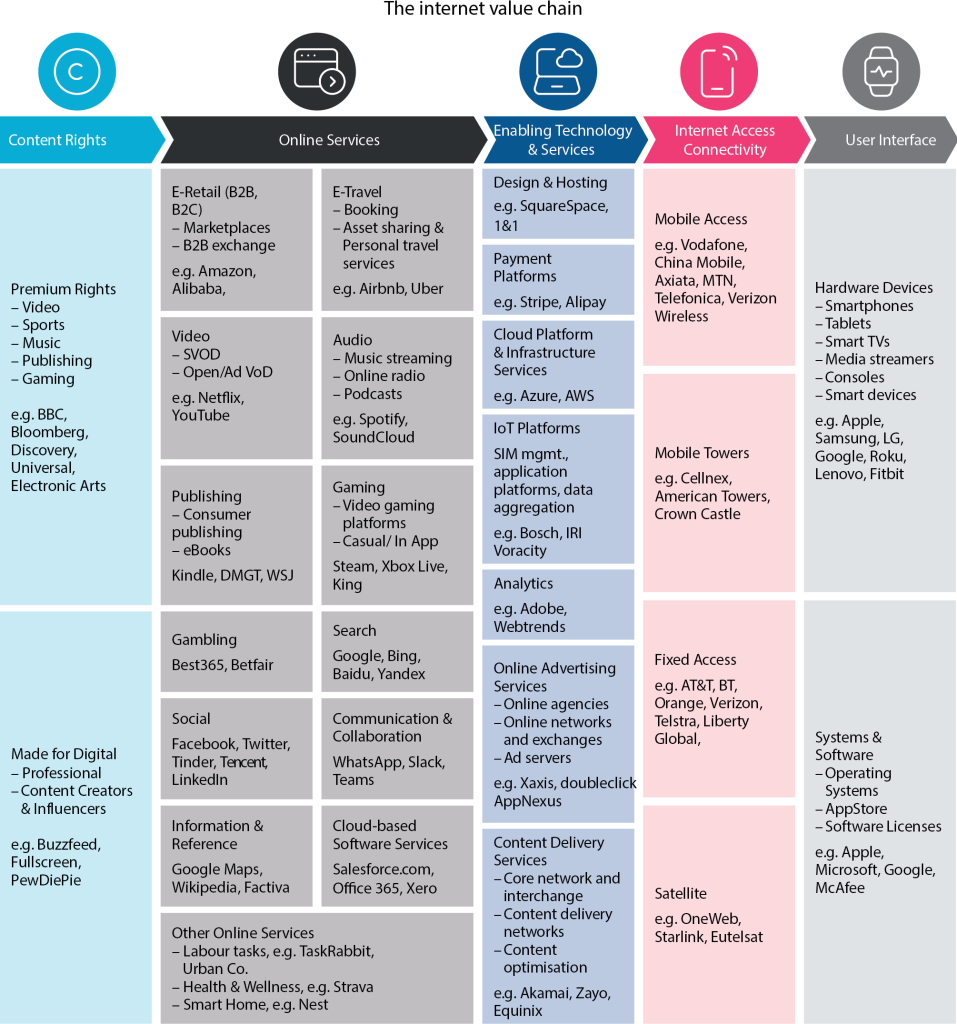

The internet value chain overall continues to grow at a steady 15 percent per year, and shows no sign of slowing down. Future developments may be less about the next big service, and rather about the emergence of entirely new, parallel ecosystems.

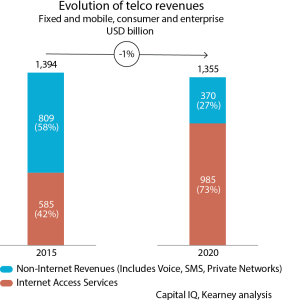

While the internet access service revenues have increased significantly from USD 585 billion in 2015 to USD 985 billion in 2020, this growth has been more than offset by the decline in non-internet-related services, primarily private data networks and declining voice revenues, which have historically been higher-margin services relative to the more commoditized internet access services. As a result, total telecom operator revenues for fixed and mobile services combined have declined slowly over the period, at a rate of 1 percent per annum.

This revenue and margin loss is being compounded by the large cloud companies directly buying and investing in international capacity to connect data centers, circumventing what has traditionally been a telecom operator service.

In some markets, regulators have reserved spectrum bands for private enterprise 5G networks to enable campus networks and specific 5G applications to be developed, such as highly automated, connected factories.

This creates an opportunity for the network equipment vendors, especially those with fully virtualized products, and the hyperscale platforms to now compete for this business, and bring their global scale to local implementations. The online-services-enabling technology and content rights segments, dominated by Meta (FKA Facebook), Google, and Netflix have been making reasonable returns of between 10 percent and 15 percent, at the cost of the telco operators, that is the internet access connectivity segment that invest, provide, and enhance the infrastructure.

It is hardly a new thesis, but the GSMA in its recent report, The Internet Value Chain 2022, reiterates that the current, unbalanced state of affairs between operators and online service providers, if not addressed, could soon affect the global growth of the internet itself. Should that eventuality come to pass, it would be a massive worldwide problem, and while the Internet value chain is currently growing at a rate of knots, the benefits of that growth are accruing primarily within the online services sector, while those providing the technologies that underpin the delivery of such services are not getting returns and profits at the rate they deserve.

In 2020, the global internet had 4.6 billion users, equivalent to 59 percent of the population of the planet. While great swathes of the world still do not have basic connectivity, let alone broadband, the Internet has quickly become the most important globe-spanning economic system in history.

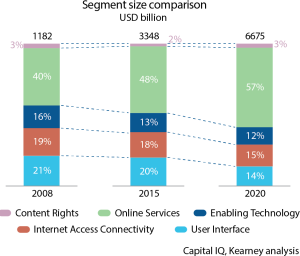

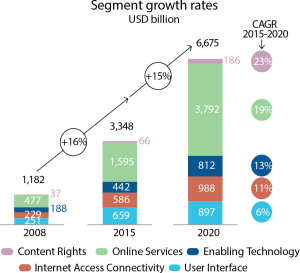

In 2020, the revenues generated by the segments that comprise the internet value chain totaled USD 6.7 trillion, more than double the USD 3.3 trillion recorded in 2015. The strongest growth over that period has been in content rights (23 percent per annum, from a low base), and online services (19 percent p.a.), which now make up 57 percent of the entire value chain in terms of revenues. The enabling technology segment grew at 13 percent, and the internet access connectivity and user interface segments at 11 percent and 6 percent, respectively.

Growth of online services since 2015 has been driven on the consumer side by the emergence of many gig-economy services, and consumers shifting more of their entertainment spend to online services, including online gaming and video streaming services, while search and social media services have continued to grow strongly. On the enterprise side, there has been a strong, ongoing migration of on-premise IT applications to cloud-based services.

The growth in entertainment has prompted increases in the activity and revenues of the content rights segment, with online video services paying more for exclusive television and movie content and the growing value of influencers creating content to reach their followers directly. Gaming content is also an active sub-segment, with the gaming platform companies increasingly investing directly.

The revenues of the enabling technology segment have also grown, offering more advanced services, including the sophisticated advertising ecosystem and advanced, hyperscale infrastructure services, enabling more services to migrate online, and the expansion of payment gateways to support the ever-growing volume of internet transactions. Revenues of the internet access connectivity segment have grown at 11 percent per year since 2015 as more people and devices are connected to the internet, but all of this growth is a substitution for previously offline or private network services (e.g., voice, MPLS, and VPN services).

The user interface segment has grown at only 6 percent per annum in total revenue. While there has been growth in the volume of connected devices, including smart TVs and smartphones, much of the growth has been at the value end, so average unit prices have declined.

In terms of overall value chain dynamics, three key trends are identified:

The largest technology players are in the process of actively expanding their footprints across the value chain, launching new online services and using their scale and existing customer bases to drive success in new segments, and also integrating along the value chain, buying up content rights players and enabling technologies, and investing in end-user devices. Super-apps emerging in some Asian markets and metaverse developments are taking a similar direction of integrated platforms and ecosystems connecting users to online services.

The majority of online services (61 percent) are paid-for rather than advertising-funded, with growth in gaming, subscription entertainment services, and enterprise cloud-based services – all driving growth. Advertising revenue growth continues to focus on search and social media services and ad-funded video services.

There is a continued shift to online, as consumers spend more time and money online. The wider trend of digitization in government and enterprises as part of a major migration from stand-alone, on-premise IT stacks to cloud-based services is driving demand for services in segments across the valuee chain, from SaaS (software as a service) applications, to cloud platform services and the connectivity services that underpin these.

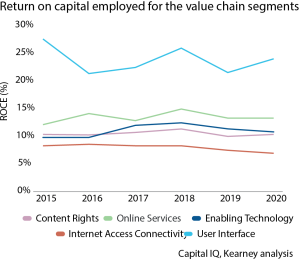

As these trends play out, a study of the economics of the sub-segments shows that the returns are not equally distributed, since each sub-segment has different underlying economics (e.g., capital intensity, scale factors, market concentration) and operates within different competition and regulatory frameworks. The online services and user interface segments are benefiting most from value-chain growth and generating the largest shareholder returns, whereas the internet access connectivity segment has generated relatively low and even single-digit returns on capital. Over the past six years, average total shareholder returns have been almost flat across the internet access connectivity segment, while other segments have at least doubled investors’ stakes and some user interface players have delivered almost six-fold returns over the same period.

At a time when a greater load is being placed on internet connectivity infrastructure, requiring network operators to increase speed, capacity, and coverage, their business model is being squeezed. First, enterprises are replacing high-margin MPLS and VPN services with more basic internet access services, resulting in an overall loss of revenue and margin for the operators. Second, the scope of operator activities is being narrowed. As virtualization of core network functions takes place, hyperscalers can develop and run these services at a global scale, playing a greater role in core service and network orchestration, while operators in many markets are separating their infrastructure (i.e., into fiber and tower companies) and selling selected assets. If these trends play out to their full extent, telecom operators risk becoming predominantly internet access providers, fulfilling the sales and service function but with significant CapEx requirements to build and maintain the access infrastructure.

In a nutshell, although the internet value chain is growing strongly, the benefits and returns are flowing principally to players in the online services segment, while the telecom operators building and running the connectivity infrastructure, which underpins these services, are not benefitting as strongly as one might expect. Although the operators continue to invest in extraordinarily complex networks that enable the entire ecosystem, the low returns raise questions about the robustness of continued investment in capacity, coverage, and speed of the networks to connect internet users with services. Business leaders and policymakers need to consider the interdependence of the many services making up the internet to ensure that market distortions, regulatory requirements, or other factors do not limit the ability of participants across the internet ecosystem to make sufficient returns and that the right incentives are in place to promote the long-term growth of the value chain and to realize the full potential of technology and service innovation.

You must be logged in to post a comment Login