Trends

Global PC shipments’ double-digit crash in Q3

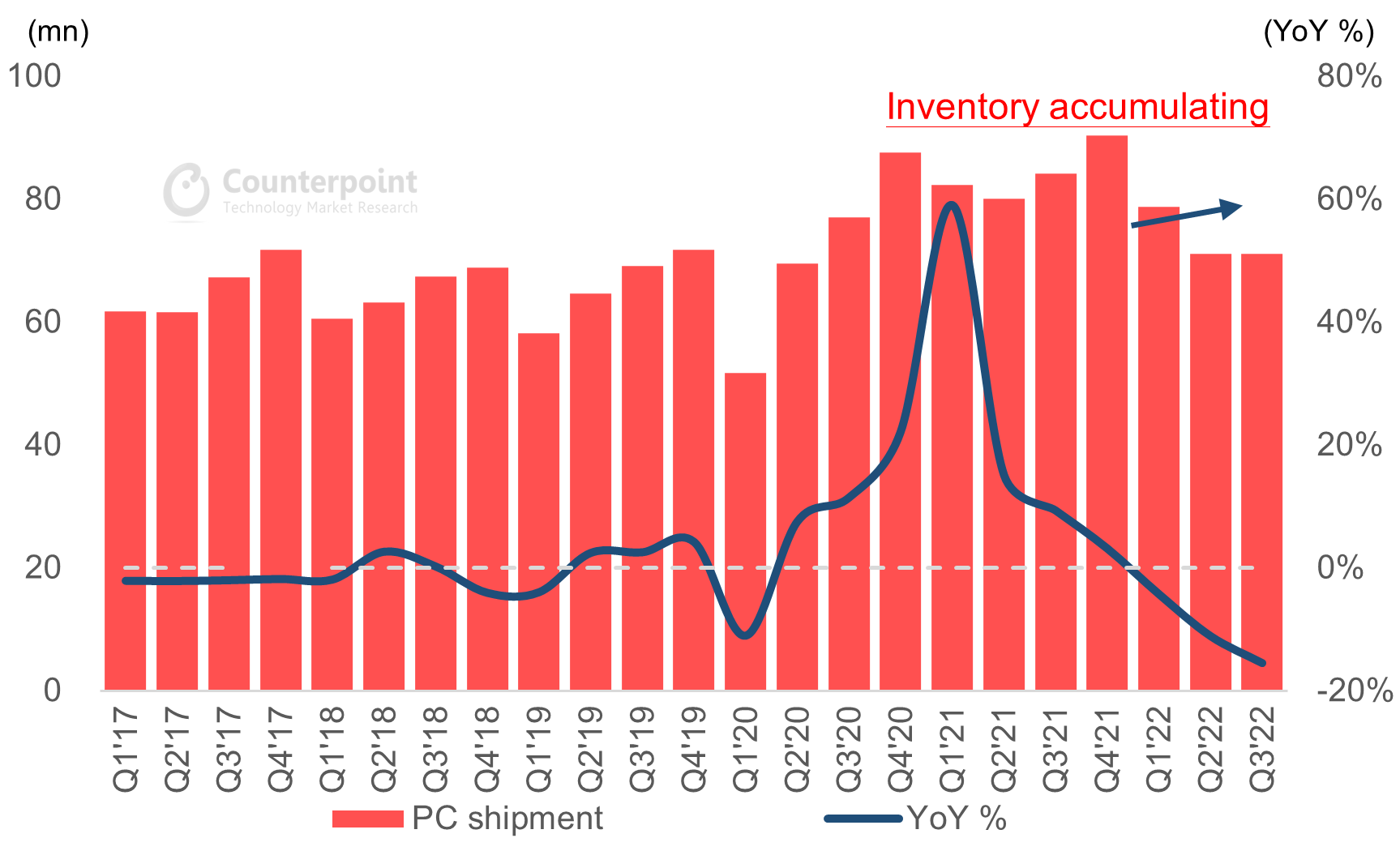

Global PC shipments fell 15.5% YoY in Q3 2022 to reach 71.1 million units recording another wave of huge YoY declines after the severe annual and sequential falls in Q2, according to Counterpoint Research data. The Q3 2022 decline was largely due to demand weakness across both consumer and commercial markets, which was mainly driven by global inflation. Despite components shortage issues being largely resolved, OEMs and ODMs are holding a relatively conservative view on Q4 2022 and first half of 2023.

The lull in PC demand continued in the quarter despite broad promotional activities from major OEMs, especially for consumer product lines. In addition, inventory digestion processes have been activated to deal with abnormally high levels as we enter the second half of the year. Although it is the season of peak consumer device sales, PC OEMs believe the destocking process will continue into 2023. Based on our conversations with supply chain members, especially with components suppliers, the largest inventory numbers were in Q3 2022 and will likely begin to decline in coming quarters but there is uncertainty within the supply chain on when shipment growth will restart.

Global PC Inventory Accumulation Since 2022

Lack of consumer demand in the back-to-school season, shrinking enterprise purchasing due to economic uncertainty and increasing promotional events all created a drag on Average Selling Price (ASP) growth momentum and also impacted PC market revenue.

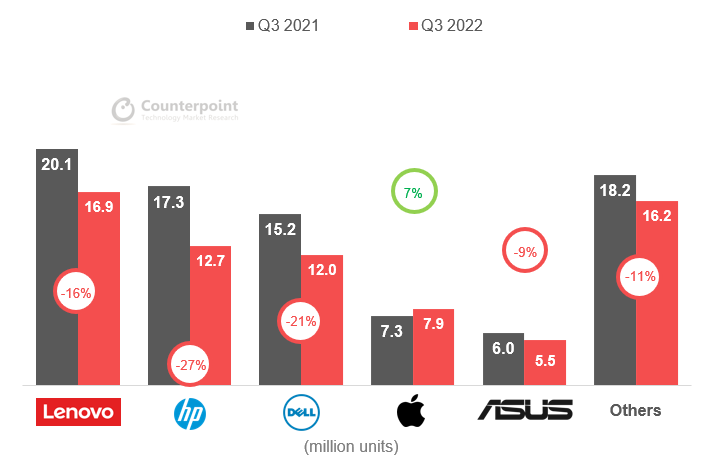

Apple reported a counter-market 7% YoY shipment growth amid muted market momentum, thanks to its new product launch in late Q2 with shipments refilled after the China lockdowns in Q2 that interrupted ODM manufacturing schedules. Meanwhile, Asus reported a 9% YoY shipment decline in the quarter, reflecting a relatively resilient performance due to its enterprise focused strategy, in line with management’s target of outperforming shipment in 2022.

Lenovo booked a 16% YoY decline, largely in-line with the global PC market, consumer demand weakness was partly offset by enterprise spending. Its 23.7% market share remains flattish compared to last year, reflecting Lenovo’s strong position efforts to cope with a shaky market.

HP took an 18% share in Q3 with 12.7 million unit shipments. This is the second quarter of lower than 20% market share by HP since 2016, largely due to its higher consumer mix, which meant it exited Q3 with a 26.5% YoY decline.

Dell also reported more than a 20% YoY shipment decline with and 17% market share. Its 12 million units were a bit higher than Q3 2020, right before Dell began to benefit from working style changes post the initial waves of COVID.

Global PC Shipment by Vendor, Q3 2022

PC market unlikely to grow until H2 2023

Overall, global PC shipments in the second half of 2022 will still be comparatively higher than the level before Covid broke out. However, Chip maker AMD claimed that PC market weakness already caused negative impacts to its results and outlook; while the management of Taiwan OEMs Acer and Asus, both shared their views that the PC industry will not recover until H2 2023.

Looking into 2023, the sky is still covered by dark clouds. We are also adjusting our 2022 shipment forecast to a 13% YoY decline on soft PC demand. Among all PC product segments, we believe Arm-based PCs and gaming PCs are poised to weather the market downturn best, with the help from Apple’s M-series offerings as well as incremental R&D efforts from chip makers and the wider ecosystem.

CT Bureau

You must be logged in to post a comment Login