Trends

Biggest cloud data security trends to watch

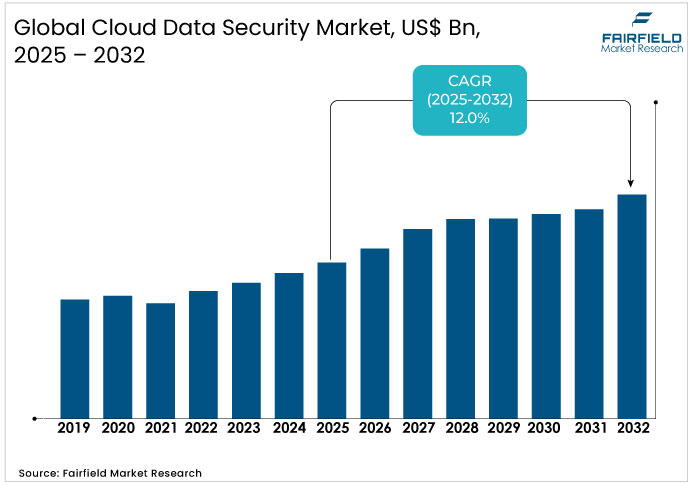

The Cloud Data Security Market is valued at USD 38.7 billion in 2025 and is projected to reach USD 85.5 billion, growing at a CAGR of 12.0% by 2032.

Cloud Data Security Market Summary: Key Insights & Trends

- Solutions dominate the global cloud data security market with over 60% share, driven by integrated encryption, access control, and threat intelligence platforms.

- Services rapidly gain share as enterprises adopt managed and co-managed detection solutions to address growing skill shortages and evolving cyber risks.

- Large enterprises hold over 70% share, leveraging scale and governance frameworks to ensure consistent compliance and safeguard vast data assets.

- SMEs continue increasing share through SaaS and co-managed models, enabling affordable and agile cloud security adoption across diverse industries.

- IT and Telecom lead with over 20% share, while Healthcare and Life Sciences expand steadily as data protection in telehealth intensifies.

- Fully managed services account for over 50% share, preferred for automated monitoring, while co-managed offerings gain traction among regulated enterprises.

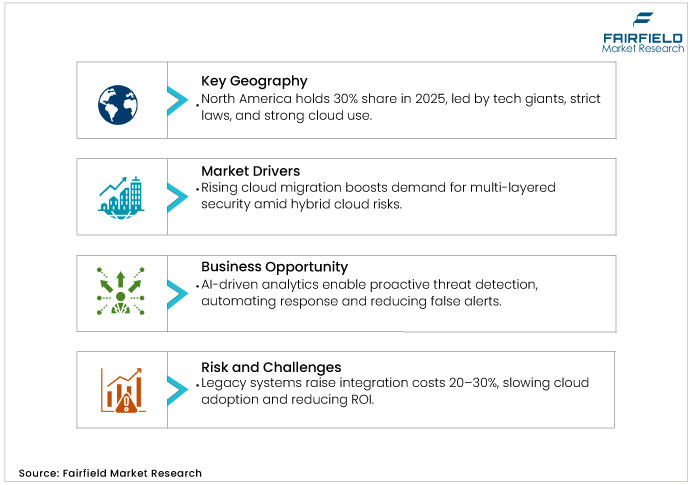

- North America retains leadership with over 30% share, supported by mature infrastructure and strong regulatory enforcement across cloud ecosystems.

Asia Pacific rapidly expands regional share as hyperscaler investments and government-led digital transformation initiatives boost cloud security demand.

Key growth drivers

Cloud migration surge drives robust demand for advanced data security solutions

The cloud data security market is expanding rapidly as organizations migrate their operations to cloud platforms, driven by the scalability and flexibility these environments offer. However, the growing adoption of hybrid and multi-cloud architectures has heightened exposure to security vulnerabilities, prompting demand for multi-layered protection frameworks.

Industry analyses indicate that by the early 2020s, more than 80% of enterprise workloads had moved to cloud environments, significantly boosting the need for advanced security solutions. This trend aligns with principles of resource optimization, as businesses realize operational cost savings of 30–50% from cloud adoption that offset initial cybersecurity investments. Furthermore, stringent data protection regulations such as GDPR and CCPA have accelerated the implementation of security-by-design approaches.

Rising cyber threats intensify global focus on cloud data protection

Cyber threats represent a perennial challenge, with theoretical risk assessment models such as NIST frameworks highlighting the probabilistic nature of attacks in distributed systems. The cloud data security market responds by embedding proactive defenses, as breach costs averaged $4.45 million globally in recent years. This driver is justified by the asymmetry between attacker sophistication and defender preparedness; ransomware and phishing evolve via AI, targeting cloud misconfigurations. Organizations counter through behavioral analytics and anomaly detection, reducing incident response times by up to 50%. Theoretically, game theory illustrates this as a zero-sum contest, where investments in threat intelligence yield asymmetric returns in resilience, sustaining market momentum.

Key restraints

Legacy Infrastructure Challenges Impede Seamless Integration of Cloud Data Security

Legacy infrastructure poses theoretical silos that hinder seamless cloud data security market integration, as per systems theory emphasizing interoperability challenges. Migrating monolithic applications to cloud environments often incurs 20-30% higher costs due to compatibility issues, deterring SMEs. This restraint stems from architectural mismatches, where outdated protocols clash with modern APIs, prolonging deployment cycles and eroding ROI.

Global shortage of cloud security talent restrains market adoption and growth

A theoretical human capital deficit restricts market penetration, with demand for cloud-savvy professionals outpacing supply by 3.5 million roles globally, according to (ISC)² surveys. Organizations face operational bottlenecks as untrained teams overlook subtle threats such as shadow IT. This curtails adoption, particularly in resource-constrained sectors, amplifying vulnerability exposure.

Cloud data security market trends and opportunities

AI and Machine Learning drive predictive intelligence in cloud data security

Advancements in AI-driven analytics present transformative potential in the cloud data security market, enabling proactive threat neutralization over retrospective forensics. Cognitive computing theories posit that machine learning algorithms can discern subtle patterns in vast datasets, theoretically preempting anomalies such as insider threats through unsupervised clustering. This opportunity arises from the deluge of telemetry data in clouds, where traditional rules-based systems falter, justifying AI’s role in automating incident triage and reducing false positives. In practice, natural language processing enhances log analysis, uncovering contextual risks in unstructured data flows. Conceptually, reinforcement learning optimizes response playbooks, adapting to adversary tactics in real-time simulations. Empirical trajectories suggest that federated learning preserves privacy while aggregating insights across tenants, mitigating data silos.

Emerging regions and new verticals unlock growth avenues for cloud security

Untapped markets in developing regions offer scalability avenues, driven by digital inclusion initiatives. Diffusion of innovations theory explains how tailored solutions bridge adoption gaps, theoretically accelerating uptake via localized compliance features. This opportunity is justified by rising internet penetration, which amplifies cloud dependencies in underserved sectors such as agriculture and education, demanding affordable, modular protections. Strategically, partnerships with telcos facilitate edge security, extending coverage to remote deployments. In theoretical constructs, network effects amplify value as ecosystems mature, drawing in late adopters through proven ROI. Patterns indicate that vertical-specific adaptations, such as HIPAA-aligned tools for healthcare, yield premium pricing.

Segment-wise trends & analysis

Integrated security solutions lead, while managed services gain rapid momentum globally

Solutions dominate the cloud data security market, capturing the lion’s share through integrated platforms that encompass encryption, access management, and threat intelligence tools. This leadership stems from their ability to deliver end-to-end visibility, theoretically aligning with zero-trust principles that verify every transaction irrespective of origin. Competitive positioning favors incumbents such as Cisco and Microsoft, who bundle solutions with native cloud integrations, outpacing fragmented offerings by reducing deployment friction.

Services emerge as the fast-growing segment, propelled by demand for managed detection and response amid skills shortages. Underlying drivers include the complexity of evolving threats, where outsourced expertise theoretically minimizes dwell times via 24/7 monitoring. Growth trajectories project accelerated adoption in SMEs, as co-sourced models democratize access to advanced forensics, enhancing competitive edges through cost-shared innovations.

Large enterprises dominate adoption while SMEs accelerate with scalable cloud security tools

Large enterprises lead with over 70% share in 2025, leveraging scale to implement comprehensive governance frameworks that safeguard vast data troves. This dominance reflects theoretical economies of scope, where centralized policies streamline compliance across global operations, positioning leaders such as IBM to consolidate market influence via enterprise-grade scalability.

Small and medium enterprises (SMEs) represent the emerging powerhouse, driven by affordable SaaS models that abstract complexities of in-house security. Trajectories indicate rapid uptake fueled by digital acceleration, theoretically empowering agility without prohibitive upfront investments. Competitors differentiate via user-friendly dashboards, capturing share by addressing SME-specific pain points such as budget constraints and rapid scaling needs.

IT and telecom lead while healthcare and life sciences drive growth

IT and telecom spearhead the market, holding over 20% share in 2025, as connectivity demands fortified perimeters against DDoS and interception risks. Leadership arises from sector-specific protocols that theoretically interweave security into 5G infrastructures, enabling giants such as Oracle to fortify network edges with AI-orchestrated defenses.

Healthcare and life sciences emerge as high-growth verticals, catalyzed by telemedicine surges that expose patient data to breaches. Drivers encompass regulatory pressures such as HIPAA, theoretically mandating granular access logs to preserve trust. Competitive landscapes favor adaptable players such as Dell, who integrate biometric verifications, gaining traction through vertical-tailored resilience.

Fully managed services prevail while co-managed models redefine cloud security operations

Fully managed services command over 50% of the cloud data security market in 2025, excelling in hands-off operations that delegate expertise to providers for seamless threat mitigation. This primacy aligns with delegation theories, where specialization theoretically optimizes resource allocation, allowing firms such as HITACHI to dominate via SLA-backed uptime guarantees.

Co-managed offerings surge as an emerging model, appealing to hybrid preferences where clients retain oversight alongside provider support. Growth is underpinned by customization needs in regulated industries, theoretically balancing control with efficiency. Positioned for expansion, innovators such as Okta excel by enabling granular delegations, fostering collaborative ecosystems that enhance adaptability.

Regional trends & analysis

North America leads global cloud data security with mature infrastructure

North America commands over 30% of the global cloud data security market in 2025, driven by the presence of major technology giants and widespread cloud adoption across enterprises of all sizes. The region benefits from mature digital infrastructure, stringent regulatory requirements, and high awareness of cybersecurity risks among organizations. The U.S. Department of Justice Data Security Program introduces additional compliance layers for telecommunications firms, generating opportunities for automated policy-mapping solutions.

US cloud data security market – 2025 snapshot & outlook

The U.S. leads global cloud security adoption, with over 89% of companies depending heavily on cloud systems for business operations. Government initiatives supporting digital transformation and smart infrastructure projects drive substantial public sector investments in cloud security solutions. The growing remote work culture and international business partnerships fuel demand for scalable security frameworks capable of protecting distributed operations. Major cloud security vendors, including Google, IBM, and Microsoft, maintain headquarters in the U.S., providing competitive advantages through proximity to innovation centers and regulatory bodies. Enterprise spending on cloud security solutions continues to accelerate as organizations prioritize data protection against sophisticated cyber threats.

Asia Pacific emerges as fastest growing hub for cloud data security

Asia Pacific represents the fastest-growing regional market with a projected CAGR, driven by rapid economic digitization and government-supported smart city initiatives. Countries including China, India, Japan, and South Korea are implementing comprehensive digital transformation strategies requiring robust cloud security infrastructure. The region benefits from significant hyperscaler investments, with major cloud providers establishing new data centers and cloud regions across key markets.

China cloud data security market – 2025 snapshot & outlook

China commands a 38.7% share of the Asia-Pacific cloud computing market, with government initiatives promoting cloud adoption while maintaining data sovereignty requirements. The “east data west computing” strategy relocates compute workloads to energy-abundant provinces, creating opportunities for distributed security solutions. Domestic cloud providers maintain significant market share while pursuing global expansion, necessitating comprehensive security frameworks that meet both local and international compliance requirements. Tightening data export regulations creates demand for security solutions that ensure data localization while enabling business operations across cloud environments.

India cloud data security market – 2025 snapshot & outlook

India emerges as the fastest-growing market in Asia Pacific, catalyzed by the GI Cloud program and substantial hyperscaler investments. The country’s accelerating digital transformation initiatives, expanding startup ecosystem, and increased cloud investments by enterprises drive substantial security solution demand. Government digitization programs and the growing fintech sector create requirements for comprehensive data protection frameworks. AWS’s significant investment commitments and expanding data center footprint demonstrate confidence in the market’s long-term growth potential, while regulatory frameworks continue evolving to support secure cloud adoption.

Europe strengthens cloud data security through regulation and data sovereignty focus

Europe maintains a significant market presence with growth driven by stringent data protection regulations and sovereignty requirements. The General Data Protection Regulation and evolving Network and Information Security Directive shape procurement criteria favoring providers with data localization options and transparent audit trails. Countries including Germany, France, and the U.K. implement national cloud security certification frameworks while working toward common European standards through the European Union Cybersecurity Certification Scheme.

Germany cloud data security market – 2025 snapshot & outlook

Germany leads European adoption in manufacturing sectors, implementing comprehensive cloud security solutions to protect industrial data and intellectual property. The country’s Cloud Computing Compliance Controls Catalog (C5) provides national certification standards that guide enterprise procurement decisions. Manufacturing companies increasingly adopt cloud-native security platforms to protect Industry 4.0 initiatives and connected factory environments. Strong regulatory compliance requirements drive investments in automated policy management and continuous monitoring solutions that ensure adherence to data protection standards.

France cloud data security market – 2025 snapshot & outlook

France emphasizes cloud sovereignty through SecNumCloud certification and investments in nationally hosted cloud zones supporting critical infrastructure projects. The Health Data Hosting (HDS) regulation creates specific requirements for healthcare sector cloud security implementations. Government initiatives promoting smart city development and digital public services drive demand for security solutions meeting strict data localization requirements. The country’s focus on protecting critical national infrastructure generates opportunities for specialized security providers offering compliance-ready solutions for regulated industries.

Competitive landscape analysis

The players in the cloud data security market are focusing on strategic partnerships to enhance interoperability and threat intelligence sharing. This approach addresses fragmented ecosystems, where multi-vendor integrations reduce silos by 40%, as evidenced by recent AWS-Microsoft alliances. Such collaborations mitigate risks in hybrid clouds, enabling faster innovation cycles. Moreover, investments in AI-driven analytics, spurred by a 2024 Ponemon breach surge, position firms to preempt attacks.

Emerging regulations such as the EU’s DORA will elevate compliance costs by 15-20%, while M&A activities consolidate capabilities, as seen in Oracle’s 2025 acquisitions. Early movers will benefit from ecosystem lock-in, while latecomers may face premium pricing pressures. Fairfield Market Research

You must be logged in to post a comment Login