Buyers

Banking in telecom

The spread and boom of telecom is well known in India. With 512.26 million internet subscribers, as of June 2018, India ranks as the world’s second-largest market in terms of total internet users.

For long have they been eyeing the banking business, eager to leverage their enormous distribution network. Just like in African countries, lower smartphone prices are driving the digitization of cash and transactions.

On January 7, 2014, the Committee on Comprehensive Financial Services for Small Businesses and Low Income Households, headed by Nachiket Mor, submitted its final report recommending the formation of a new category of banks called payments banks.

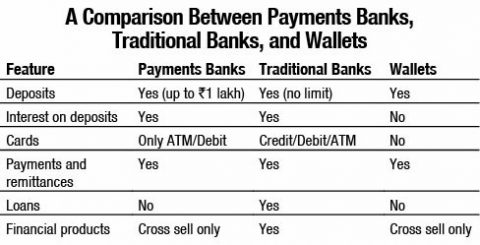

A payments bank is a differentiated bank with the specific objective of financial inclusion by providing small savings accounts and payments/remittance services.

Payments banks aim to service the unbanked, under-banked, and bottom of the pyramid (BoP), especially migrant workers and those from lower income households, as well as bring them into the formal financial system.

With advent of payments banks, RBI seeks to increase the penetration level of financial services to the remote areas of the country, which are not catered to by traditional banks because their brick-and-mortar structure renders their profitability negative in rural/low income areas.

For banks, the primary source of income is lending and deposits. A payments bank cannot lend, and deposits per account are restricted to Rs 1 lakh. Hence, payments banks can sustain only if they are technology-driven with focus on number of customers; hence, key benefits being cashless technology-driven transactions, which eliminate black money and promote Digital India. This has supported growth of fintech in the country since now adoption of technology in banking is being spearheaded by payments banks. Just like the m-pesa experiment with Safari Telecom in Africa has yielded great results, telecoms in India hope to replicate the success.

For banks, the primary source of income is lending and deposits. A payments bank cannot lend, and deposits per account are restricted to Rs 1 lakh. Hence, payments banks can sustain only if they are technology-driven with focus on number of customers; hence, key benefits being cashless technology-driven transactions, which eliminate black money and promote Digital India. This has supported growth of fintech in the country since now adoption of technology in banking is being spearheaded by payments banks. Just like the m-pesa experiment with Safari Telecom in Africa has yielded great results, telecoms in India hope to replicate the success.

Current Indian scenario

Of the 41 applicants, 11 were given provisional payments bank licenses by RBI. These include Aditya Birla Nuvo Limited, Airtel M Commerce Services Limited, Cholamandalam Distribution Services Limited, India Department of Posts, Fino PayTech Limited, National Securities Depository Limited, Reliance Industries Limited, Shri Dilip Shantilal Shanghvi, Paytm Payments Bank Limited, Tech Mahindra Limited, and Vodafone m-pesa Limited. The active payments banks are Aditya Birla Payments Bank, Airtel Payments Bank, India Post Payments Bank, Fino Payments Bank, Jio Payments Bank, Paytm Payments Bank, and NSDL Payments Bank.

Bharti Airtel launched India’s first live payments bank, Airtel Payments Bank in March 2017. Paytm Payments Bank, India Post Payments Bank, Fino Payments Bank, and Aditya Birla Payments Bank have also launched services. Cholamandalam Distribution Services, Sun Pharmaceuticals, and Tech Mahindra have surrendered their licenses.

Despite the near-saturation of certain markets, there is still ample room for growth in mobile financial services in India. The future for payments bank seems bright for now.

The views in the article are independent and have been formulated by experience of author in payments bank industry and researching the information available

on web.