Trends

Nearly 500 smartphone brands exit market as competition intensifies

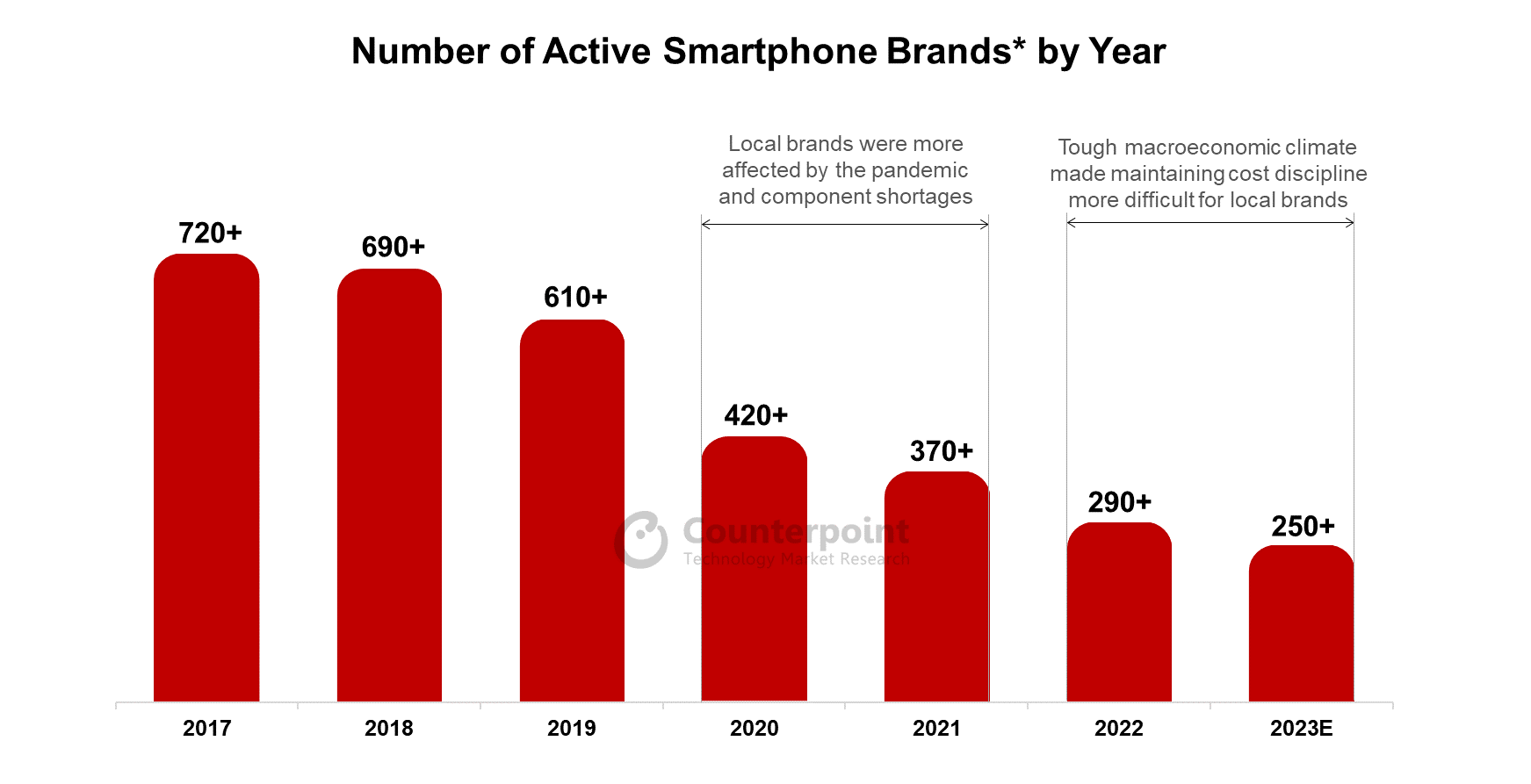

At its peak in 2017, the global smartphone market saw more than 700 brands fiercely competing. Fast forward to 2023 and the number of active brands (that have recorded sell-through volumes) is down by two-thirds to almost 250, according to Counterpoint’s Global Handset Model Sales Tracker, which has been tracking sales of these brands across more than 70 key countries.

A maturing user base, improving device quality, longer replacement cycles, economic headwinds, supply-chain bottlenecks and major technological transitions such as 4G to 5G have gradually whittled down the number of active brands and their volumes over the years. For example, local smartphone brands, once known as “local kings”, like Micromax in India and Symphony in Bangladesh, have lost significant share or even exited over the last five years.

Decline of local brands

Strikingly, the decline in the number of active brands is coming largely from local brands, while the number of global brands has remained mostly consistent. Most local brands operate in lower price bands and in regions that have fragmented markets across wide geographies, like Asia-Pacific, Latin America and Middle East & Africa.

Brands lag in R&D and marketing efforts

In a rapidly evolving smartphone industry, small brands have struggled to keep up with big brands across many fronts. While big brands have continued to invest in R&D, manufacturing and capacity building, small brands have been largely dependent on white-label devices. Furthermore, large promotional and marketing events and big-name brand ambassador tie-ups from sports and movies are commonplace for big brands, which most small brands don’t have the resources to do.

Evolving customer needs

Small brands capitalized on the market’s transition from 2G to 3G/4G, benefitting from strong entry-tier demand, particularly in Africa, Asia and Latin America. However, the needs of the average mobile phone consumer have been evolving since and the user base has matured. Therefore, there is now a greater demand for better specifications and design, brand value and ecosystem integration.

Unable to keep up with growing Tier-1 Chinese brands

The rise of Chinese brands like Xiaomi, OPPO and vivo has also accelerated the decline of small brands. Chinese brands have been able to introduce significantly better smartphones at aggressive price points, providing customers better value for their money.

Small brands more affected by industry headwinds

From the COVID-19 pandemic and component shortages to the ongoing global economic slowdown, multiple headwinds have affected smartphone brands across the board in the recent past. For big brands, it has been relatively easier to shore up profit margins in this market environment. But small brands have struggled to keep operations running.

Going forward, the number of smartphone brands will continue to decrease, and large global brands will be in the best position to adapt to all the macroeconomic headwinds and technological transitions in the market.

Key takeaways

A maturing smartphone user base, better R&D innovations by big brands, expansion of competing bigger brands and tough macroeconomic conditions have been the key drivers for this market consolidation trend. Therefore, small-scale or even incumbent brands looking to survive in this market need to invest in R&D to differentiate, be prudent with their target segments and marketing strategies, track the competition closely and identify gaps and opportunities to succeed. Counterpoint Research

You must be logged in to post a comment Login