Trends

China’s Q1 2024 smartphone sales rise 1.5% YoY

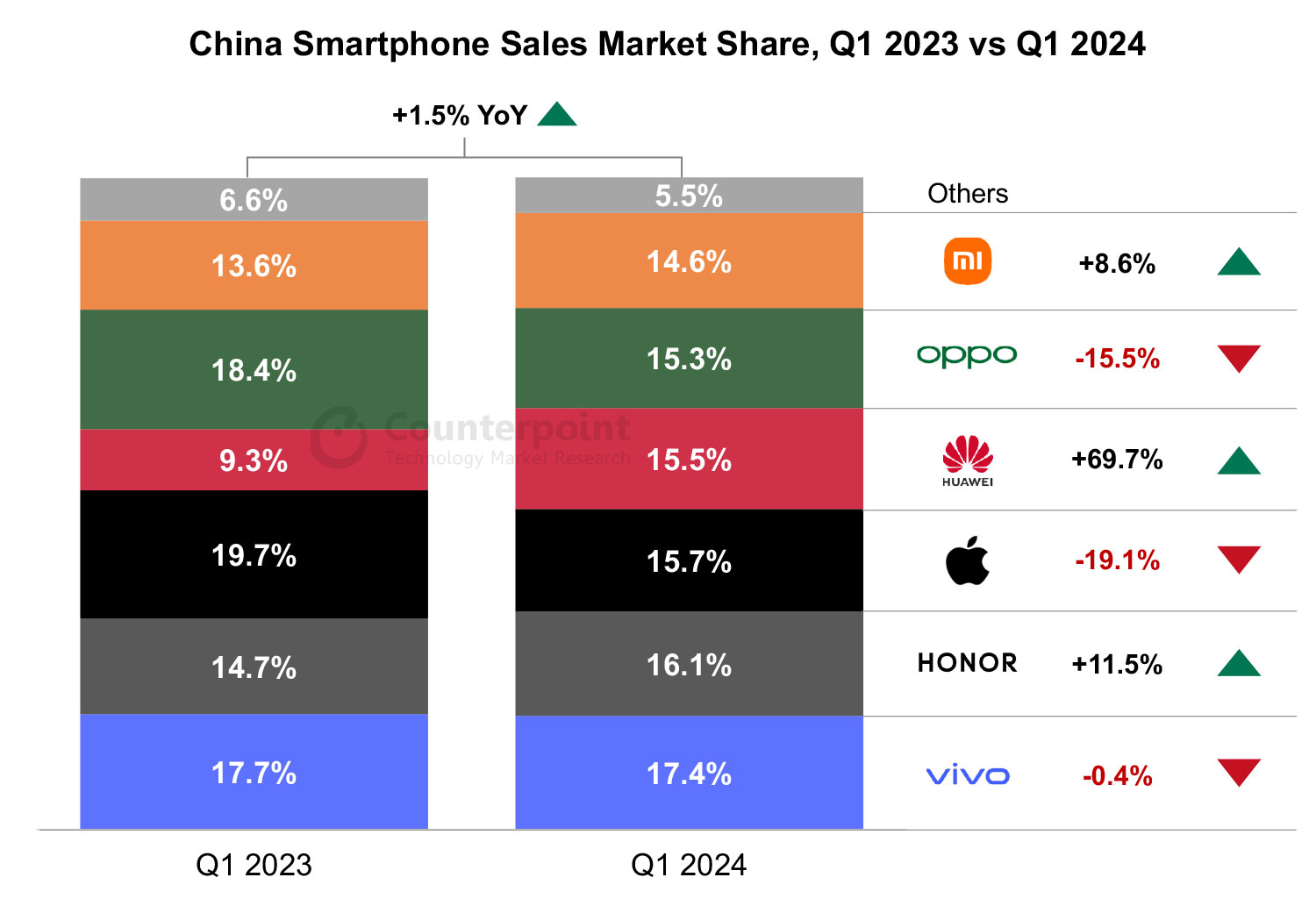

China’s smartphone sales grew 1.5% YoY in Q1 2024, marking the second consecutive quarter of positive YoY growth, according to Counterpoint’s Market Pulse Service. Huawei stood out as the best performer among all OEMs during Q1, growing 69.7% YoY. Huawei’s growth was largely attributed to the successful launch of the 5G-capable Mate 60 series as well as its enduring brand reputation, helping it to gain a massive share in the $600+ premium segment. Despite Huawei’s comeback, HONOR still managed to grow 11.5% YoY in Q1 driven by its popular models, such as the X50 and Play 40, and its expansion in offline channels.

Commenting on the market dynamics, Associate Director Ethan Qi said, “Momentum seems to be building on a recovery as China’s smartphone sales continued their growth trajectory and grew 4.6% QoQ in Q1 2024. The sales promotions during the Chinese New Year festivities were the biggest growth driver. The average weekly sales during the four weeks leading up to the Chinese New Year saw a robust growth of 20% when compared to a normal week, according to Counterpoint’s China Smartphone Weekly Model Sales Tracker.”

Further commenting on the market dynamics, Senior Analyst Mengmeng Zhang said, “Q1 2024 was the most competitive quarter ever, with only 3% points separating the top six players in terms of market share. Smartphone OEMs compete fiercely during the festive period, finalizing various marketing and promotional strategies well in advance. In particular, Chinese OEMs, with their ample cost-effective offerings, capitalize on the surge in sales in the low-end segment as migrant workers purchase more affordable, budget smartphones when returning home for the holidays. This trend further narrowed the market share gap among major players.”

Commenting on OEM performance, Senior Research Analyst Ivan Lam said, “vivo gained the top spot this quarter with 17.4% share driven by strong sales of the Y35 Plus and Y36 models in the low-end segment and the S18 in the mid-end segment. HONOR ranked second with a 16.1% share, followed by Apple with a 15.7% share. Apple’s sales were subdued during the quarter as Huawei’s comeback has directly impacted Apple in the premium segment. Besides, the replacement demand for Apple has been slightly subdued compared to previous years.”

Looking forward, Lam saw the possibility of an iPhone recovery: “We are seeing slow but steady improvement from week to week, so momentum could be shifting. For the second quarter, the possibility of new color options combined with aggressive sales initiatives could bring the brand back into positive territory; and of course, we are waiting to see what its AI features will offer come WWDC in June. That has the potential to move the needle significantly longer term.”

Counterpoint Research estimates low single-digit YoY growth for China’s smartphone market in 2024. The advent of generative AI has already seen Chinese OEMs integrating such features into their flagship devices. We anticipate smartphone OEMs will continue to explore new AI applications, with these advancements further trickling down to the mid-end segment. Counterpoint Research

You must be logged in to post a comment Login