Headlines of the Day

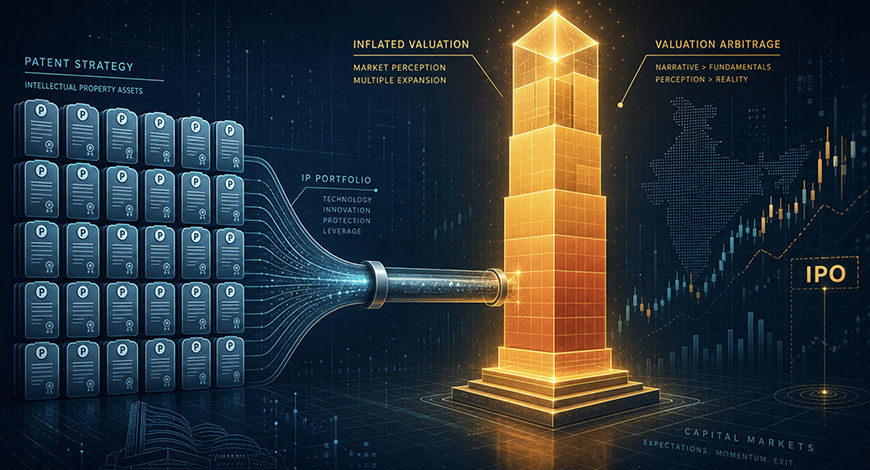

The cheapest valuation arbitrage in Indian capital markets

Run the numbers, and Jio’s patent strategy becomes almost elegant.

Filing roughly 900 PCT applications through the Patent Cooperation Treaty costs between $8,000 and $10,000 each. Call it $8 million all in, a rounding error for a company preparing to raise $4 billion at an IPO. In exchange, Jio Platforms leaped from #320 to #20 in WIPO’s global rankings, landing itself in a press release alongside Huawei, Samsung, Qualcomm, and Google.

That press release, if it moves Jio’s valuation multiple even modestly, from telco territory toward tech territory, could be worth tens of thousands of crores. The return on that $8 million filing spend might be the highest-yield investment Reliance makes this decade.

This isn’t a patent story. It’s an arbitrage story.

The multiple gap that makes this worth doing

Telecom businesses trade at roughly 6–8x EV/EBITDA. Technology businesses trade at 20–30x. The gap exists because markets believe tech companies compound through intellectual property; telcos are infrastructure businesses that depreciate. Jio straddles this divide uncomfortably, it is, structurally, a network operator, but its IPO ambitions require a technology valuation.

The question Reliance’s bankers needed to answer was: what moves the multiple? Revenue growth? Margins? Both are constrained by competitive dynamics in the Indian telecom. User counts? Already saturating. What remained was narrative, and narrative, in capital markets, runs on proxies. A WIPO Top 20 ranking is exactly the kind of third-party signal that shows up in an analyst’s comparable-company framework, in an institutional investor’s pre-read, in a business journalist’s 200-word IPO preview.

Jio’s management understood this. The $8 million was spent not on innovation but on credentialing.

The number that punctuates the story

There is one data point in Jio’s own filings that collapses the narrative, and it sits quietly in the DRHP: a 14.8 percent patent grant rate.

Grant rates matter because they represent external validation, a patent examiner at a national office, who has no stake in Jio’s IPO, reviewing the application against prior art and deciding whether it describes something genuinely novel. Jio’s own historical grant rate, before the filing surge, ran at approximately 98 percent. The crash to 14.8 percent is not due to rounding. It suggests that a large share of the newly filed applications describe things that already exist, or that are obvious extensions of existing technology.

This has an explanation: speed. Consolidating patents across Reliance subsidiaries and filing hundreds of PCT applications in a compressed window necessarily sacrifices quality for volume. Filing is mechanical; inventing is not. Internal sources at Reliance have noted, with some bewilderment, that the applications went out “with little internal review.” The WIPO ranking reflects what was filed, not what was invented.

At $8,000–$10,000 per application, a 14.8 percent grant rate means Jio is spending roughly $54,000–$68,000 in filing costs for every patent that actually gets granted. That is inefficient intellectual property management by any measure. It is, however, entirely rational if the goal is a ranking rather than a portfolio.

What WIPO’s methodology cannot see

WIPO’s annual rankings are a count. They do not assess novelty. They do not assess commercial value. They do not assess whether the applications describe real inventions or recombinations of prior art. WIPO says as much, clearly, in its own methodology documentation, a fact that seems not to have complicated the language Jio’s management chose at last Friday’s AGM.

At that AGM, and in the DRHP released the same day, the ranking was presented as evidence of “R&D productivity and intellectual property depth.” This framing requires treating the ranking as a quality signal, even though WIPO designed it only as a volume signal. The distinction is not subtle. It is the entire point.

Anubhab Sarkar, managing partner at Triumvir Law, puts it plainly: “A rise of this kind reflects, at least in part, a shift in filing strategy rather than necessarily a change in underlying innovation.” What makes this notable is the context: R&D headcount at Reliance has been reported as “1000+” for four consecutive years. R&D spending has held at roughly 0.4 percent of revenue for years. The inputs to innovation have not changed. Only the patent filings have.

The signal SEBI should be reading

India’s capital markets regulator has, in recent years, sharpened its scrutiny of IPO disclosures, particularly around metrics that issuers present as performance indicators. The question worth asking is whether a WIPO ranking derived from a filing surge, rather than from underlying innovation, constitutes a material misrepresentation when presented in a DRHP as evidence of technological depth.

This is not an abstract concern. Institutional investors pricing Jio’s IPO will, in part, be pricing its intellectual property position. If that position is overstated, if the 14.8 percent grant rate signals that the bulk of the PCT portfolio will not survive examination, then the valuation case for a technology multiple weakens. The market will eventually find out; grant decisions from national patent offices will accumulate over the next three to five years. The question is whether investors are told enough, at the IPO stage, to price that risk.

The DRHP discloses the filing and grant counts. It does not prominently contextualize the historical grant rate or explain the shift in filing strategy. It presents the WIPO ranking as “an important external recognition of Jio Platforms’ R&D productivity.” A reader who did not already know that WIPO rankings are volumetric would not come away knowing it.

Why this matters beyond Jio

The deeper issue is what happens to India’s technology credibility when its largest conglomerate treats patent filings as a marketing instrument. India has spent years building a genuine innovation story, ISRO, fintech infrastructure, and a growing deep-tech startup ecosystem. That story is grounded in what works: UPI, NAVIC, the IIT-lab-to-company pipeline.

Jio’s surge in filings doesn’t destroy that story. But it muddies the metrics that the world uses to measure it. If WIPO’s Top 20 now includes an entry that got there through consolidation and speed-filing rather than invention, then the ranking means something different than it did before, for Jio and for every Indian company that might legitimately appear there in future years.

A few million dollars for a “top innovator” narrative is a bargain. The cost it imposes on Indian tech credibility is harder to quantify, and nobody filing the PCT applications had to put it on a balance sheet.

The main shift here is that the original leads with “this is suspicious” and builds toward the financial motive. This version leads with the financial logic up front, helping the reader understand why the strategy is rational before questioning whether it’s legitimate. That inversion makes the critique land harder, because you’ve already granted the strategic intelligence before pulling it apart.

CT Bureau

You must be logged in to post a comment Login