Company News

Nokia earnings in Q4 2023 lower as customer spending slows

Nokia Corporation Financial Report for Q4 and full year 2023-A summary.

Improving order intake and cash flow at the end of a challenging year

- Net sales declined 21% y-o-y in constant currency (-23% reported) in Q4 as macroeconomic uncertainty continues to pressure operator spending. Full year net sales declined 8% y-o-y in constant currency (-11% reported).

- In Q4 the environment remained challenging however there are now signs of stabilization with improving order trends.

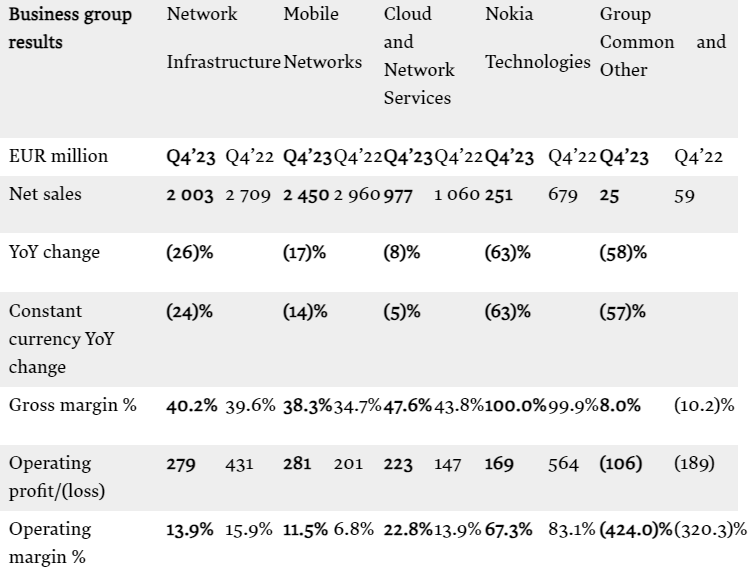

- Comparable gross margin in Q4 declined by 40bps y-o-y to 43.1% (reported declined 100bps to 41.8%). Significant improvements in Mobile Networks and Cloud and Network Services were offset by lower contribution from Nokia Technologies which benefited from a significant one-off in the prior year.

- Q4 comparable operating margin declined 70bps y-o-y to 14.8% (reported down 220bps to 9.6%), demonstrating the resilience of our profitability relative to the net sales decline. 2023 comparable operating margin 10.7% (reported 7.6%)

- Q4 comparable diluted EPS of EUR 0.10; reported diluted EPS of EUR -0.01. Full year EUR 0.29 and EUR 0.12 respectively. Q4 reported EPS impacted by an operating model change that led to non-cash remeasurement of deferred tax assets.

- Q4 free cash flow positive EUR 1.7bn, net cash balance EUR 4.3bn. Full year free cash flow EUR 0.8bn.

- Board proposes dividend authorization of EUR 0.13 per share and initiates two year EUR 600 million buyback program.

- Nokia expects full year 2024 comparable operating profit of between EUR 2.3 billion to 2.9 billion and free cash flow conversion from comparable operating profit of between 30% and 60%.

Pekka Lundmark, President And CEO, “In 2023 we saw a meaningful shift in customer behavior impacting our industry driven by the macro-economic environment and high interest rates along with customer inventory digestion. This led to our full year net sales declining by 8% in constant currency. Proactive action across our organization meant we were able to protect our profitability while continuing to invest in R&D and we delivered a comparable operating margin of 10.7% for the full year. This was a resilient performance considering the challenging environment and lower contribution from our high margin patent licensing business as some renewals remained outstanding.

Looking specifically at the fourth quarter those same factors drove a net sales decline of 21% y-o-y in constant currency. Encouragingly we saw improvements in our gross margin across several of our businesses which, combined with continued cost discipline, helped us to deliver a strong comparable operating margin of 14.8%. In addition, we have seen a significant improvement in order intake in the fourth quarter, particularly in Network Infrastructure, indicating at least some improvement in the overall spending environment.

We delivered well in 2023 against our strategic pillar of growing in Enterprise with 16% net sales growth in constant currency and this customer segment now accounts for over 10% of our group net sales. Growth in the fourth quarter was muted at -3% in constant currency as we faced a tough comparison period. We continue to have strong momentum in this segment and expect another year of double-digit growth in 2024.

In Network Infrastructure we made important progress in a number of areas in the quarter. We received further webscale orders for our IP Routing business which supports our expectations of significant growth in webscale in 2024. In the fourth quarter we also saw good progress in the US government initiatives in Fixed Networks and we continue to expect these programs to increasingly benefit our net sales in the second half of 2024 and into 2025. The fourth quarter also saw us sign a new and significant customer in Asia for our Fixed Wireless Access products. In Optical Networks we continue to have good momentum and our new PSE-6s solutions are proving their capabilities in the field; recent live network trials set a new record of 800Gbps transmission on a single wavelength over 6 600km.

Mobile Networks net sales performance continued to be challenging in the fourth quarter, but we did see a further important improvement in gross margin which benefited from a product mix shift towards software. AT&T’s announcement in December to move to a largely single-sourced RAN network was a disappointing development. It does not reflect the technological competitiveness we have achieved with our products as evidenced by our significant increase in RAN market share in recent years. I firmly believe we have the right strategy in place for Mobile Networks to create value for our shareholders into the future with opportunities to gain share, diversify our business and achieve a double-digit operating margin longer-term.

Our Cloud and Network Services business had a strong year. We had a slight decline in net sales for the full year, but we made progress on profitability with a largely stable gross margin and improved operating margin. The business continued to rebalance its portfolio, with the divestment of its Device Management and Service Management Platform businesses in December. During 2023, we led the industry trend towards programmable networks with the launch of our Network as Code platform which now has 9 commercial agreements and we also achieved our first commercial deal for 5G Core as a service to CSPs.

In Nokia Technologies, we signed significant long-term deals with both Apple and Samsung in 2023 and we also signed a deal with Honor late in the year. I am also pleased that we have now signed a multi-year agreement with OPPO and we are close to concluding another agreement in China. After these, we are in the final stages of our smartphone license renewal cycle with only one other, recently expired, major agreement outstanding. This provides long-term stability to our Nokia Technologies business which will continue to focus on growing our licensing run-rate in new growth areas including automotive, consumer electronics, IoT and multimedia. I remain confident that with growth in these areas we can return to an annual net sales run-rate of EUR 1.4 to 1.5 billion in Nokia Technologies in the mid-term.

A clear positive in the fourth quarter was our cash flow performance. We generated EUR 1.7 billion of free cash flow as we saw a significant improvement in working capital in the quarter supported by a partial prepayment of a licensing agreement. We ended the year with a net cash position of EUR 4.3 billion. The Board is proposing a dividend of EUR 0.13 per share in respect of the financial year 2023 and considering we now hold excess cash at the end of the year, the Board is also instituting a new share buyback program of EUR 600 million to be executed in the next two years.

Looking ahead, we expect the challenging environment of 2023 to continue during the first half of 2024, particularly in the first quarter. However, we are now starting to see some green shoots on the horizon, with improving order intake for Network Infrastructure and some of the specific deals we have won. This is expected to drive a strong improvement in Network Infrastructure net sales growth in the second half of 2024 which we believe, even with a challenging first half, will drive solid growth for the full year. In Mobile Networks, we expect top line challenges in 2024 related to a more normalized pace of investment in India and the AT&T decision. We do expect further improvement in gross margin and then in the second half we will start to see more benefits from our cost savings program. At the Nokia level, we currently estimate that we will deliver comparable operating profit of between EUR 2.3 and 2.9 billion in 2024. We also target to deliver an improved free cash flow performance with conversion of between 30% and 60%.

I want to thank all our people for their resilience and determination to deliver these results and executing on our corporate strategy in what can only be described as a highly challenging market environment.

Financial results

Shareholder distribution

Dividend

The Board of Directors proposes that the Annual General Meeting 2024 authorizes the Board to resolve on the distribution of an aggregate maximum of EUR 0.13 per share to be paid in respect of the financial year 2023. The authorization would be used to distribute dividend and/or assets from the reserve for invested unrestricted equity in four installments during the authorization period, in connection with the quarterly results, unless the Board decides otherwise for a justified reason.

Under the authorization by the Annual General Meeting held on 4 April 2023, the Board of Directors may resolve on the distribution of an aggregate maximum of EUR 0.12 per share to be paid in respect of financial year 2022. The authorization will be used to distribute dividend and/or assets from the reserve for invested unrestricted equity in four installments during the authorization period, in connection with the quarterly results, unless the Board decides otherwise for a justified reason.

On 25 January 2024, the Board resolved to distribute a dividend of EUR 0.03 per share. The dividend record date is on 30 January 2024 and the dividend will be paid on 8 February 2024. The actual dividend payment date outside Finland will be determined by the practices of the intermediary banks transferring the dividend payments.

Following this announced distribution of the fourth installment and executed payments of the previous installments, the Board has no remaining distribution authorization.

Share buyback program

Nokia’s Board of Directors is initiating a share buyback program under the current authorization from the Annual General Meeting to repurchase shares, with purchases expected to begin in Q1. The program targets to return up to EUR 600 million of cash to shareholders in tranches over a period of two years, subject to continued authorization from the Annual General Meeting.

In February 2022, Nokia’s Board of Directors initiated a share buyback program to repurchase shares to return up to EUR 600 million of cash to shareholders in tranches over a period of two years. The second EUR 300 million phase of the share buyback program started in January 2023 and was completed in November 2023. Under this phase, Nokia repurchased 78 301 011 of its own shares at an average price per share of approximately EUR 3.83. The repurchases reduced the Company’s unrestricted equity by EUR 300 million and the repurchased shares were cancelled in November 2023.

Outlook

| Full Year 2024 | |

| Comparable operating profit1 | EUR 2.3 billion to EUR 2.9 billion |

| Free cash flow1 | 30% to 60% conversion from comparable operating profit |

The outlook, long-term targets and all of the underlying outlook assumptions described below are forward-looking statements subject to a number of risks and uncertainties as described or referred to in the Risk Factors section later in this release. Along with Nokia’s official outlook targets provided above, below are outlook assumptions by business group that support the group level outlook.

| Nokia business group assumptions | ||

| Net sales growth (constant currency) | Operating margin | |

| Network Infrastructure | +2% to +8% | 11.5% to 14.5% |

| Mobile Networks | -15% to -10% | 1.0% to 4.0% |

| Cloud and Network Services | -2% to +3% | 6.0% to 9.0% |

Nokia provides the following approximate outlook assumptions for additional items concerning 2024:

| Full year 2024 | Comment | |

| Seasonality | H2 weighted | Nokia expects Q1 net sales in its networks businesses (consisting of Network Infrastructure, Mobile Networks and Cloud and Network Services) to show an approximately normal seasonal decline sequentially. Since 2016 the average Q1 sequential decline in sales has been -23%. Nokia expects significant seasonality in profit generation in 2024 with low sales coverage to weigh on operating profit in Q1, particularly in MN and CNS. The company then expects progressive improvement in these businesses through the year. |

| Nokia Technologies operating profit | at least

EUR 1.4 billion |

Nokia assumes operating profit in 2024 for Nokia Technologies of at least EUR 1.4 billion which assumes resolution of outstanding renewals and includes catch-up net sales related to prior periods. Nokia expects cash generation in Nokia Technologies to be EUR 700 million below operating profit in 2024 due to prepayments received in 2023. From 2025 onwards Nokia expects greater alignment between cash generation and operating profit in Nokia Technologies. |

| Group Common and Other operating expenses | EUR 350 million | This includes central function costs which are expected to be largely stable at approximately EUR 200 million and an increase in investment in long-term research to approximately EUR 150 million. |

| Comparable financial income and expenses | EUR 0 to negative EUR 100 million | |

| Comparable income tax rate | ~25% | |

| Cash outflows related to income taxes | EUR 500 million | |

| Capital Expenditures | EUR 600 million |

2026 Targets

On 12 December 2023, as a conclusion to Nokia’s long-range planning process, the company decided to lower its comparable operating margin target to be achieved by 2026 from the prior at least 14% to at least 13%. Nokia still sees a path to achieving the at least 14% comparable operating margin target but considering the current market conditions in Mobile Networks, this was deemed a prudent change. Nokia sees further opportunities to increase margins beyond 2026 and believes this 14% target remains achievable over the longer term.

| Net sales | Grow faster than the market |

| Comparable operating margin1 | ≥ 13% |

| Free cash flow1 | 55% to 85% conversion from comparable operating profit |

The comparable operating margin target for Nokia Group is built on the following assumptions by business group for 2026:

| Network Infrastructure | 12 – 15% operating margin |

| Mobile Networks | 6 – 9% operating margin |

| Cloud and Network Services | 7 – 10% operating margin |

| Nokia Technologies | Operating profit more than EUR 1.1 billion |

| Group common and other | Approximately EUR 300 million of operating expenses |

Risk factors

Nokia and its businesses are exposed to a number of risks and uncertainties which include but are not limited to:

- Competitive intensity, which is expected to continue at a high level as some competitors seek to take share;

- Our ability to ensure competitiveness of our product roadmaps and costs through additional R&D investments;

- Our ability to procure certain standard components and the costs thereof, such as semiconductors;

- Disturbance in the global supply chain;

- Accelerating inflation, increased global macro-uncertainty, major currency fluctuations and higher interest rates;

- Potential economic impact and disruption of global pandemics;

- War or other geopolitical conflicts, disruptions and potential costs thereof;

- Other macroeconomic, industry and competitive developments;

- Timing and value of new, renewed and existing patent licensing agreements with smartphone vendors, automotive companies, consumer electronics companies and other licensees;

- Results in brand and technology licensing; costs to protect and enforce our intellectual property rights; on-going litigation with respect to licensing and regulatory landscape for patent licensing;

- The outcomes of on-going and potential disputes and litigation;

- Timing of completions and acceptances of certain projects;

- Our product and regional mix;

- Uncertainty in forecasting income tax expenses and cash outflows, over the long-term, as they are also subject to possible changes due to business mix, the timing of patent licensing cash flow and changes in tax legislation, including potential tax reforms in various countries and OECD initiatives;

- Our ability to utilize our Finnish deferred tax assets and their recognition on our balance sheet;

- Our ability to meet our sustainability and other ESG targets, including our targets relating to greenhouse gas emissions;

CT Bureau

You must be logged in to post a comment Login