Company News

Apple US iPhone inventory rises above H1 2025 tariff build-up levels

Apple’s weeks of inventory are climbing higher than even the tariff build up in H1 2025, recovering after a period of difficulty in meeting iPhone 17 demand in the US, according to Counterpoint’s US Monthly Smartphone Inventory Tracker.

The memory crunch is pushing smartphone OEMs in the US to build inventory faster in H1 2026 than during H1 2025, when fears of looming tariffs shifted demand significantly.

According to Counterpoint’s US Monthly Smartphone Inventory Tracker, Apple’s weeks of inventory are climbing higher than even the tariff build up in H1 2025, recovering after a period of difficulty in meeting iPhone 17 demand in the US. With higher inventory levels, Apple will be able to save on margins by taking advantage of H1 2026 memory chip pricing. This will also help the brand maintain pricing through the rest of 2026 and allow it to continue to capture US market share as the year progresses. In March and April of 2025, ahead of ‘Liberation Day’, Apple was proactive and began pushing large volumes into the US through May. The brand built up enough cushion to make it to the iPhone 17 launch should China tariffs be implemented again and rotated much of its US production to India. Despite the strong shipments in March and April 2025, Apple’s channel inventory is still higher YoY.

Meanwhile, Samsung’s inventory is rising higher in April YoY partially due to shipments for the S26 series beginning in January, despite the delayed launch, and remained strong throughout Q1 2026. Samsung’s elevated inventory levels can only be partially explained with increased flagship shipments. Samsung has been pushing significant volumes of the Galaxy A16 and Galaxy A17 devices, despite weakness in the prepaid segment in the US. While the prepaid space is in a downturn, this buildup only makes sense if Samsung is trying to load up on H1 2026 memory pricing to make a longer run through the rest of the Galaxy A16 and A17 lifecycle and avoid having to raise prices. Front loading the lifecycle for these two models will allow Samsung to manage reduced LPDDR4 memory availability.

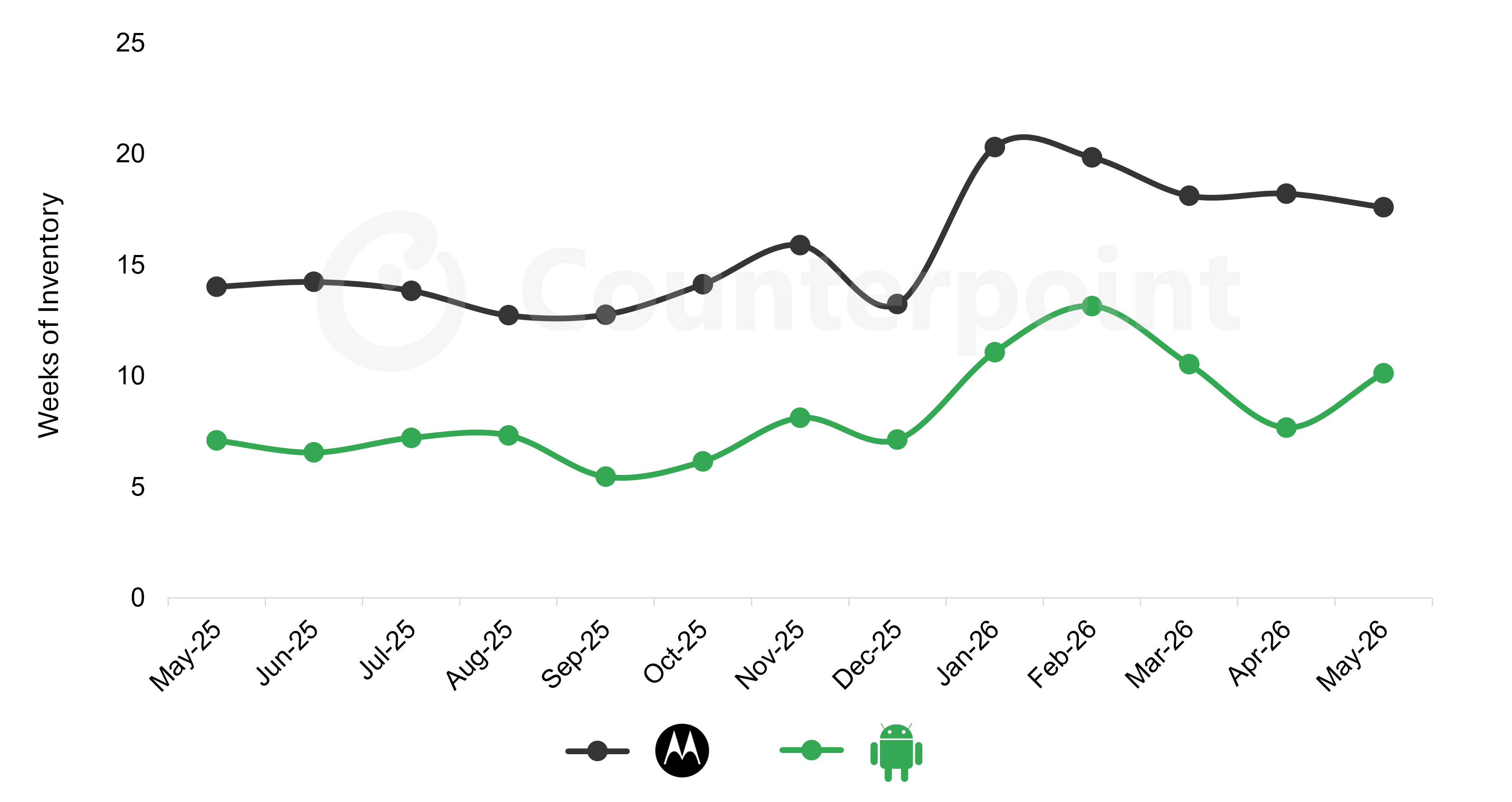

Motorola’s inventory exceeds the aggregate weeks of inventory for Android OEMs, reaching an all-time high in the US.

Motorola vs Android US Weeks of Inventory (May 2025 – May 2026)

Motorola’s persistently higher weeks of inventory relates to the higher reliance on national retail channels, increasing store counts to stock. Weeks of inventory are outpacing levels during the same period in 2025 by a significant margin. Increased shipments began in Q4 2025 and have persistently remained elevated despite lower sell-through figures. The situation for Motorola is more precarious than that of other OEMs. Most of its US market share is drawn from the prepaid space in lower price bands. Its three largest volume drivers rely on LPDDR4 memory chips. The brand was already forced to raise prices on some of these models. Now, it is attempting to keep its prepaid models in stock throughout the rest of the year while it tries to carve out a spot for itself in the premium postpaid space with the Razr Fold, which is getting a $1,700 discount at T-Mobile during the launch period.

The AI-driven memory chip crisis is still not getting the attention that tariffs did from the general public, with many carrier store reps still unaware of the BOM cost challenges. However, this situation is shaping up to be far more impactful than the tariff announcements were in the US. Both the memory chip crisis and impact of demand being pulled forward from 2026 into 2025 combined are having a compounding effect. All major US OEMs reacted to tariffs in one way or another to mitigate price increases. The situation altered supply chains, manufacturing countries of origin and inventory management. Now, memory considerations are again reshaping roadmaps, product management lifecycles, and procurement strategies in ways not seen during the smartphone era. Back-to-back years of volatility are forcing unprecedented reactions from smartphone OEMs.

The chip shortage stretched OEMs during the COVID-19 pandemic. However, with memory, there is little reprieve in sight with memory chip players unable to keep up with AI-driven demand, even with new production lines coming online in 2027. Samsung has been forced to roll out some price increases on devices across its full portfolio from lower priced devices to its most premium foldables. Despite having its own memory division, it still must source from Micron and fight for memory chip allocation internally. So far, price increases have yet to impact sales in the US in a major way. Should they be forced to increase pricing on low-end A series devices during the transition to LPDDR5, volumes may begin to fall as price-sensitive consumers may opt to delay upgrades. Holding periods overall would likely climb. Motorola’s story is quite similar. The OEM has its volumes secured for its prepaid volume drivers, but it is just as exposed due to its reliance on prepaid to maintain US market share. So far, Apple is positioned the strongest, in the US, to navigate 2026 and 2027 with extra hardware margin to play with versus its peers. It has a significant opportunity to grow its share, not just in the US, but globally as well. Counterpoint Research

You must be logged in to post a comment Login