CT’s Take

The vacuum effect

How mega-IPOs act as a structural liquidity drain, and what Jio’s listing means for India

The imminent listing of Reliance Jio’s telecom-and-media behemoth is poised to become one of the largest equity events in Asian financial history. At prospective valuations between ₹6 lakh crore and ₹10 lakh crore, it will not merely test the appetite of India’s capital markets, it will redefine their geometry. The question that deserves urgent examination is not whether investors want Jio, but what they will sacrifice to own it.

This report argues that mega-IPOs function as structural liquidity vacuums: when a single issuance absorbs a meaningful fraction of the market’s annual investable surplus, capital cannot be in two places at once. The primary market’s gain is the secondary market’s gravity. History from Tokyo to Frankfurt, Hong Kong to Riyadh confirms the pattern. India, constrained by a four-percentage-point gap between deposit growth and credit expansion, enters this episode with less margin for error than most.

“When equity supply turns into a gush, the broader pool of market liquidity tends to dry up. When the primary market claims the final dregs of investable cash, gravity asserts itself on the secondary market.” — Market Strategist

THE PRESSURE BUILDING AT THE SUMMIT

Jio’s scale in context

Reliance Jio Infocomm, the crown jewel of Mukesh Ambani’s empire, is not simply a telecom operator. It is a vertically integrated digital ecosystem, encompassing mobile broadband for over 450 million subscribers, JioCinema’s streaming catalog, JioMart’s commerce layer, and an expanding fiber-to-home network. That combination of recurring cash flows and strategic optionality has drawn comparisons to American tech conglomerates more than to traditional carriers.

Pre-IPO rounds in 2020–2021 attracted over $20 billion from the likes of Facebook (now Meta), Google, KKR, and Abu Dhabi Investment Authority, each purchasing a stake at valuations that embedded the full promise of India’s digital decade. When Jio ultimately lists, those anchor investors will be looking for an exit path, and new buyers will need to find the funds to absorb supply running into the tens of billions of dollars.

A single quarter’s earthquake

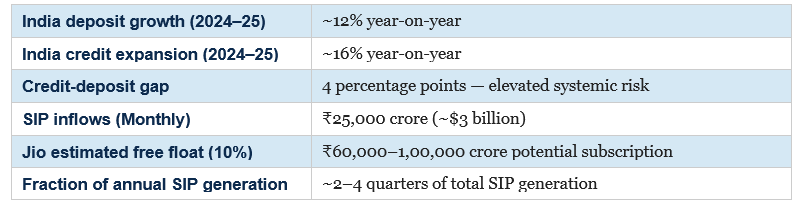

India’s domestic mutual fund industry manages roughly ₹60 lakh crore in assets under management, with systematic investment plan (SIP) inflows of approximately ₹25,000 crore per month, or ₹3 lakh crore annualised. A Jio IPO at the upper end of valuation estimates, with even a 10% free float, would require subscription money in the range of ₹60,000–1,00,000 crore. That is a single quarter’s entire SIP generation chasing one company. Anchor allocations, grey-market premiums, and institutional book-building aside, that pressure must come from somewhere, and somewhere is the secondary market.

The analogy is familiar from hydraulic engineering: if you divert a river, the original channel runs dry. Equity markets are not rivers, sentiment and velocity create their own momentum, but the underlying principle holds. Capital committed to a primary subscription cannot simultaneously support valuations in the broader index.

“Air at the top is getting thin. When the primary market claims the final dregs of investable cash, gravity asserts itself on the secondary market.”

THE MECHANICS OF A LIQUIDITY DRAIN

How IPO subscriptions strip liquidity

Understanding the liquidity drain requires disaggregating where IPO subscription money originates. In India’s retail-driven market, it comes from four principal pools: (1) bank savings and fixed deposits partially liquidated ahead of the IPO window; (2) existing equity portfolios partially sold to fund the subscription; (3) margin borrowing against existing equity holdings; and (4) fresh inflows from the diaspora and foreign portfolio investors redirected from secondary allocations.

Each source carries a secondary-market cost. Liquidating FDs creates only a modest demand impact, but selling secondary equities to fund subscriptions is a direct double blow: supply rises as sellers exit positions, and demand falls as buyers earmark cash for the IPO window. Margin lending is equally double-edged, brokerages extend credit ahead of allotment, but those lines are often drawn down against the broader margin book, tightening the pool available for leveraged secondary positions.

The allotment echo

The liquidity stress does not end at subscription close. When allotment occurs and unsuccessful applicants receive refunds, money floods back into the system, but often not to the same places it left. Retail investors who sold mid-cap positions to chase the IPO do not necessarily redeploy into those positions upon refund. They may subscribe to the next wave of IPOs, or simply hold cash as the IPO euphoria fades, leaving the secondary market structurally under-owned in the interim.

Meanwhile, institutional investors who received allotment must now decide how much of the rest of their book to pare. Benchmark index managers are forced to buy Jio the moment it enters the index family; to maintain tracking error within bounds, they must sell something else. For an IPO the size of Jio, the index rebalancing effect alone could rival, in absolute dollar terms, the free-float adjustments that roiled markets when Saudi Aramco entered the MSCI Emerging Markets index in 2019.

INDIA’S STRUCTURAL VULNERABILITY

The 4-percentage-point chasm

India’s banking system in 2024–2025 reported deposit growth of approximately 12% year-on-year against loan book expansion closer to 16%. That four-percentage-point gap, what economists call the credit-deposit (CD) ratio strain, is not a temporary aberration. It reflects a structurally under-saved economy financing its ambitions by stretching available liquidity.

The Reserve Bank of India has flagged this divergence with increasing urgency. When a banking system is already operating at elevated CD ratios, any additional drain on deposits to fund equity subscriptions compounds systemic stress. The Jio IPO, to the extent it incentivises households to redeploy fixed-income savings into equity, will not create new investable capital, it will merely migrate it from one form of productive deployment (bank lending) to another (primary equity), while leaving a vacuum in both the secondary equity market and the deposit base.

The diaspora bridge and its limits

Indian policymakers and Reliance’s investor relations team are acutely aware of this tension. One proposed bridge is the non-resident Indian (NRI) and foreign portfolio investor channel, tapping the accumulated savings of the Indian diaspora, which sends approximately $120 billion in remittances annually and controls a substantially larger stock of offshore wealth.

There is real capital available here. The diaspora’s financial assets span everything from NRE deposits at Indian banks to offshore dollar portfolios in the Gulf, Singapore, the United Kingdom, and the United States. Structuring the Jio IPO to attract significant NRI participation through ASBA-NR accounts and qualified foreign investor routes could meaningfully diversify the funding base away from the domestic secondary market.

However, diaspora capital is not unlimited, and it carries a price. Gulf-based NRIs, who represent a large cohort, hold a significant portion of their liquid wealth in local currency deposits and local equity markets, markets that are themselves sensitive to oil price cycles. When equity supply turns into a gush, even the diaspora pool $120 billion in annual remittances notwithstanding, cannot offset a simultaneous drawdown from both domestic SIP investors and institutional rebalancers. The mathematics of marginal capital allocation are unforgiving.

A single quarter’s equity issuance absorbing a meaningful fraction of annual deposit formation is a system-wide hazard. The danger is particularly elevated in India, where the banking system’s 12% deposit growth is four percentage points slower than credit expansion.

A GLOBAL RECKONING: FOUR TELECOM MEGA-IPO CASE STUDIES

Telecommunications companies have historically served as the favoured vehicle for governments to execute “people’s capitalism”, mass privatisations dressed up as national participation events. The combination of brand recognition, monopolistic heritage, and reliable cash flows made telecoms the ideal asset for drawing retail investors into equity markets for the first time. Each of the following cases illustrates a different facet of the same liquidity dynamic.

Case study 1: NTT DoCoMo, Japan, 1998

The world’s largest IPO at the time | ¥2.1 trillion (~$18.4 billion)

When the Nikkei froze in anticipation

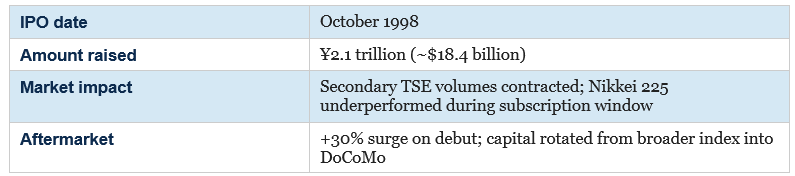

In October 1998, Nippon Telegraph and Telephone listed its mobile subsidiary, NTT DoCoMo, on the Tokyo Stock Exchange in what was, at the time, the largest initial public offering ever executed globally. The ¥2.1 trillion transaction, equivalent to roughly $18.4 billion at prevailing exchange rates, dwarfed anything the Japanese market had previously absorbed.

The liquidity drain was immediate and measurable. In the weeks surrounding the subscription period, secondary market volumes on the TSE contracted sharply as institutional investors set aside capital for the DoCoMo allotment process. The Nikkei 225 experienced an episode of unusual lethargy that market historians attribute in part to the DoCoMo gravitational field: with so much capital earmarked for the primary market, bids dried up across the broader index.

DoCoMo’s aftermarket behaviour further illustrated the crowding dynamic. The stock surged more than 30% in its first days of trading as allotted institutional investors marked positions and retail participants who missed allotment chased it in the secondary market. The capital that flooded into DoCoMo came, in no small part, from the rest of the Nikkei, particularly from other NTT group entities and large-cap industrials, which underperformed conspicuously during the same window.

Case study 2: Deutsche Telekom, Germany, 1996–2000

The ‘volksaktie’ trilogy | three tranches, one structural drain

The people’s share and the market it devoured

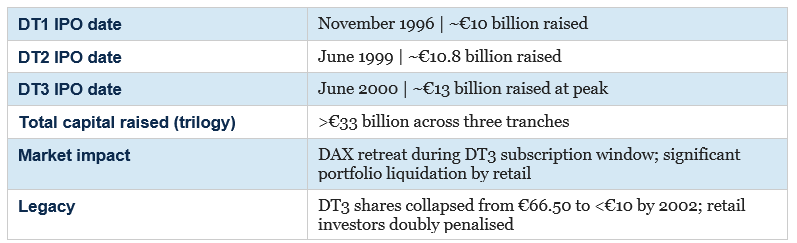

Germany’s privatisation of Deutsche Telekom produced not one but three successive mega-IPOs, DT1 in November 1996 (~€10 billion), DT2 in June 1999 (~€10.8 billion), and DT3 in June 2000 (~€13 billion at the height of the dot-com bubble), each marketed to ordinary Germans under the banner of “die Volksaktie,” the people’s share. The campaign was one of the most successful retail equity mobilisations in European history, enrolling millions of first-time shareholders.

The liquidity impact of DT1 was moderated by its novelty: German retail investors had few competing equity commitments, so the capital mobilised was largely incremental. By DT3, however, the dynamic had flipped entirely. The DAX was at or near its peak; equity allocations in German household portfolios were historically elevated; and the subscription for DT3 required investors to recycle capital from existing positions. The broader DAX retreated noticeably during the June 2000 subscription window, even as the global dot-com correction was still gathering speed.

DT3 was also the most instructive failure: priced at €66.50, the shares collapsed below €10 by 2002 as the dot-com bust accelerated. The retail investors who had liquidated diversified holdings to subscribe to DT3 suffered doubly, direct losses on Deutsche Telekom and opportunity costs from the positions they had sold to fund the subscription. The people’s share became a generational cautionary tale about the dangers of mega-IPO concentration.

Case study 3: China Mobile, Hong Kong / NYSE, 1997

Timing the storm | $4.5 billion into a collapsing regional market

When the listing date meets a macro earthquake

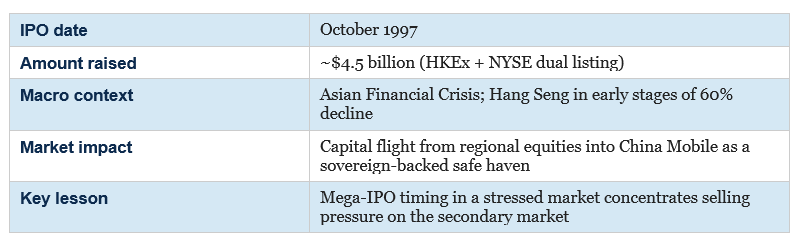

China Mobile (Hong Kong) Limited listed on the Hong Kong Stock Exchange and the New York Stock Exchange in October 1997, raising approximately $4.5 billion in one of the first major Chinese state-enterprise privatisations. The timing was unfortunate in ways that illuminate both the power and the fragility of mega-IPO liquidity dynamics.

The Asian Financial Crisis had taken hold in July 1997, crashing currencies across Thailand, Indonesia, Malaysia, and South Korea. By October, contagion was spreading visibly to Hong Kong. The Hang Seng Index was in the early stages of what would become a 60% peak-to-trough decline. Against this backdrop, the China Mobile subscription absorbed capital that Hong Kong institutions desperately needed to maintain positions across a market in freefall.

The Chinese sovereign backstop, implicit but well understood, made China Mobile an almost irresistible safe-haven trade for investors fleeing regional contagion. Capital flowed into China Mobile and simultaneously out of peripheral Hong Kong-listed equities, property companies, and regional banks. The IPO thus acted as an accelerant on the secondary market’s decline, not because it caused the crisis, but because it created a more attractive exit ramp that encouraged portfolio liquidation at exactly the wrong moment for market stability.

The parallel to India in 2026 is pointed. A Jio IPO in an environment of tightening global liquidity or elevated geopolitical risk would similarly create a “flight to quality within equities” dynamic, capital flowing into Jio as a perceived bellwether of India’s digital economy, and out of the mid-cap and small-cap segments where liquidity is already thinner.

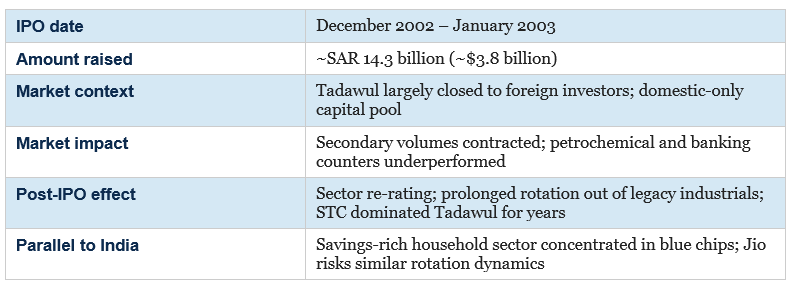

Case study 4: Saudi Telecom Company (STC), Saudi Arabia, 2003

Tadawul’s big bang | A domestic mega-IPO in a shallow market

When one IPO reshapes an entire market rrchitecture

The IPO of Saudi Telecom Company on the Tadawul (Saudi Stock Exchange) in December 2002–2003 raised approximately SAR 14.3 billion (~$3.8 billion) and remains one of the defining events in the history of Gulf capital markets. Unlike the global examples above, STC listed into a market that was, at the time, largely closed to foreign investors, making the liquidity dynamics almost entirely a function of domestic Saudi capital.

The Tadawul in 2002–2003 was a market of modest depth, dominated by a handful of banking and industrial conglomerates. STC’s arrival was seismic. With millions of Saudi nationals eligible to subscribe, and a subscription structured around a heavily discounted offering price that all but guaranteed first-day gains, the IPO triggered a mass mobilisation of household savings. Family offices, high-net-worth individuals, and pension funds alike reallocated portfolios to participate.

The secondary market impact was stark. In the months surrounding the STC IPO, trading volumes in established Tadawul listings contracted as subscription capital was locked up in the allotment process. Petrochemical and banking counters, the market’s largest constituents, drifted lower even as oil prices were supportive. Post-allotment, STC’s debut triggered a re-rating of the entire telecommunications sector and a prolonged rotation out of legacy industrial holdings that reshaped the index composition for years.

The STC case is especially instructive for India because both markets share a defining characteristic: a large, savings-rich household sector whose equity participation is concentrated in state-adjacent blue chips. When those households redirect capital into a mega-IPO, the rest of the market, including exactly the kind of growth companies that need secondary market support to fund expansion, is left competing for a diminished pool of attention and money.

WHEN THE WELL RUNS DRY, SYSTEMIC RISK AND THE INDEX EFFECT

The final dregs of investable cash

Across all four historical cases, Tokyo, Frankfurt, Hong Kong, Riyadh, the pattern is consistent. A mega-IPO does not merely redirect capital; it restructures the market’s liquidity geometry. It creates a gravitational centre that bends the trajectories of all surrounding assets. For the months straddling the listing, the IPO is the market’s conversation, its benchmark, and its buyer of last resort for its own shares. Everything else, by definition, becomes the residual.

The danger intensifies when the macro environment is already providing a headwind. In India today, the combination of elevated CD ratios, a 12% deposit growth rate that trails credit expansion by four percentage points, and a global environment of higher-for-longer rates means that the system is already operating without a significant liquidity buffer. A Jio IPO in this environment is not simply a large equity event, it is a large equity event in a system with limited shock-absorbing capacity.

The index rebalancing multiplier

One underappreciated amplification mechanism is passive fund rebalancing. India’s index ecosystem, Nifty 50, BSE Sensex, MSCI India, collectively underpins hundreds of billions of dollars in passive capital, both domestic and foreign. The moment Jio is added to these indices, which will happen rapidly given its expected market capitalisation, passive managers are mandated to buy. That buying must be funded by selling whatever they currently hold at the relevant weights.

For MSCI India in particular, the addition of a company the size of Jio would likely require the index to significantly shrink the weights of incumbents like HDFC Bank, Infosys, Reliance Industries (the parent), and ICICI Bank. Those are precisely the counters that anchor institutional confidence in Indian equities. A forced de-weighting, compressed into the trading days around index inclusion, could generate negative momentum in the very stocks that international portfolio investors use as their primary exposure to India.

Diaspora capital cannot plug all gaps

Reliance’s investment banking advisers will almost certainly structure the Jio IPO to maximise participation from offshore pools, QIB tranches allocated to sovereign wealth funds, NRI tranches marketed through Gulf and Singapore wealth management channels, and ADR or GDR components to attract Western institutional money. These measures will dilute the domestic secondary market drain, but they cannot eliminate it.

The fundamental constraint is that even the most globally oriented IPO structures still require domestic price discovery, anchor-investor confidence, and a retail subscription tranche that mobilises Indian household capital. When equity supply turns into a gush, the broader pool of market liquidity tends to dry up. The diaspora provides a longer hosepipe, but it does not conjure a second well.

The systemic hazard of a mega-IPO is not that the company fails, it is that the secondary market, stripped of the capital needed to sustain its own valuations, generates a self-reinforcing correction in the weeks and months around the primary market’s moment of triumph.

CONCLUSION: THE THINNING AIR AT THE TOP

Jio’s IPO will be a landmark event in the history of Indian capital markets, a validation of the country’s ambition to nurture world-scale digital companies and list them at home. For investors, it will represent one of the rare opportunities to buy into a genuine category-defining platform at a moment of public access.

None of that changes the structural arithmetic. NTT DoCoMo froze the Nikkei. Deutsche Telekom’s Volksaktie trilogy liquidated German retail portfolios across three successive episodes, culminating in the ruin of DT3. China Mobile’s debut accelerated capital flight from an already-stressed regional market. Saudi Telecom’s listing restructured the Tadawul’s hierarchy for a decade. Each was a success on its own terms; each exacted a price from the secondary market surrounding it.

India’s regulators, institutional investors, and policymakers would do well to approach Jio’s listing not only as a celebration but as a liquidity stress test, one whose results will be visible in mid-cap valuations, credit-deposit ratios, SIP redemption patterns, and passive fund turnover for months after the listing confetti has settled. The air at the top is getting thin. The question is whether the broader market can breathe through what comes next.

CT Bureau

You must be logged in to post a comment Login