Trends

Tokyo, Sydney and Seoul lead data centre growth in Asia-Pacific

Knight Frank, the global property advisor, has released its latest Data Centre Report in partnership with DC Byte, focussing on the APAC data centre hubs of Singapore, Hong Kong, Sydney, Shanghai, and Tokyo; and hyper- growth markets including Seoul, Mumbai, Bangkok, and Kuala Lumpur – to provide the most wide-ranging view of the region.

According to the report, APAC saw an increase of 488MW (Megawatts) of new capacity in Q1, up from 185MWinthe previous quarter, bringing the total capacity to more than 8,700MW. This growth was mostly driven by Tokyo, Sydney and Seoul, with Sydney crossing a significant threshold to become a Gigawatt market. Across the region, 203 MW of capacity was absorbed this quarter largely due to public cloud activity, a number significantly higher than the average 127 MW per quarter as previously observed in 2021.

4MW increase in IT power supply; 2.99MW of IT power capacity absorbed in Mumbai in Q1 2022

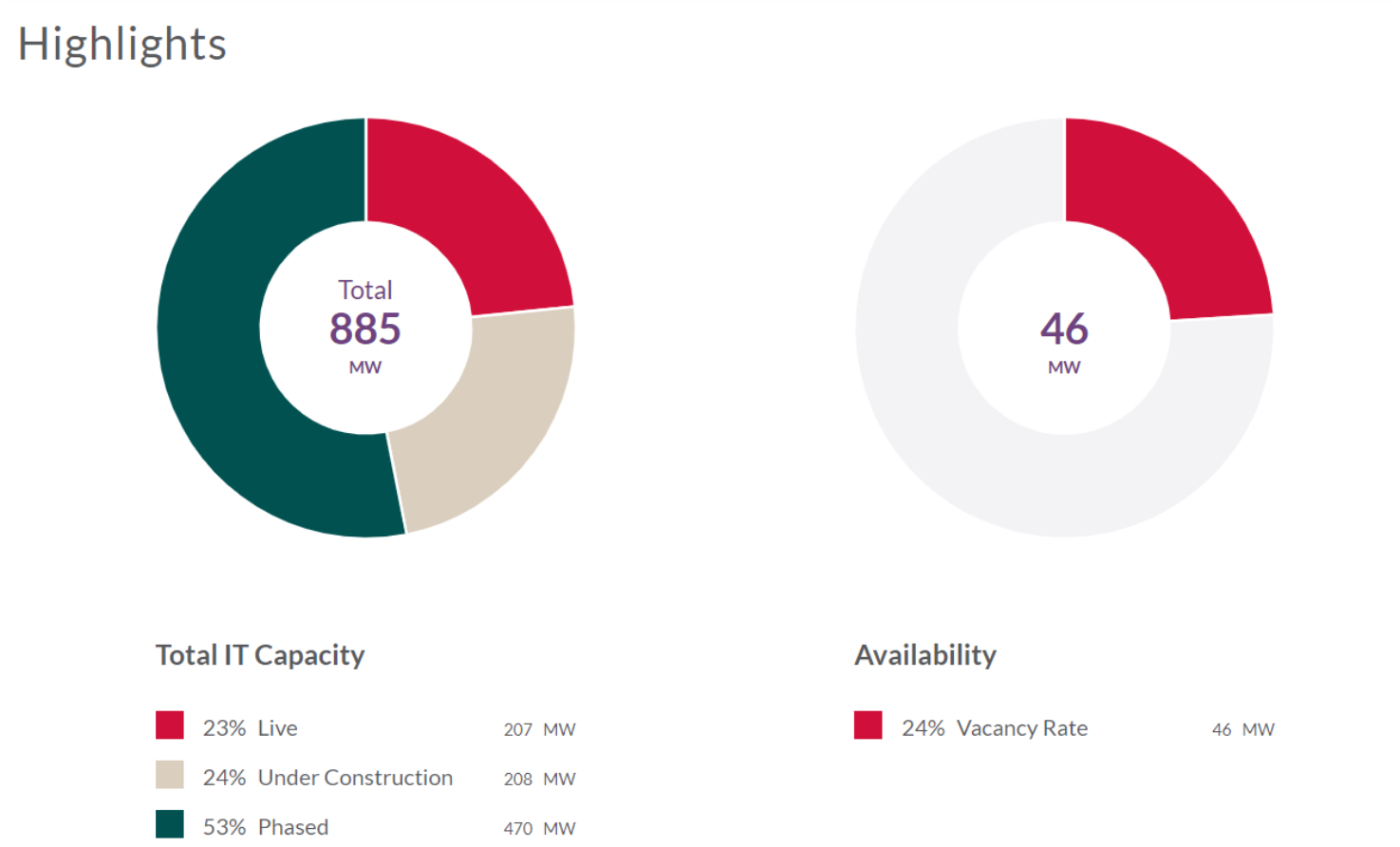

Mumbai witnessed a 4MW increase in supply in Q1 2022 which brings up the total IT capacity in the city to 885MW. The supply increase in Q1 2022 was primarily driven by Equinix’s announcement of a third facility called MB3. 2.99 MW of IT power capacity was absorbed during Q1 2022 in Mumbai.

IT POWER MW: Across key Asia Pacific markets

The chart below shows the cumulative figure of IT power since inception

| City | Live IT Power in MW (Megawatts) | Under construction IT power in MW (Megawatts) | Phased IT Power in MW (Megawatts) |

| Tokyo | 997.00 | 194.30 | 921.30 |

| Shanghai | 778.29 | 422.25 | 592.05 |

| Mumbai | 207.14 | 207.76 | 470.30 |

| Sydney | 467.58 | 236.15 | 333.20 |

| Hong Kong SAR | 410.93 | 144.00 | 309.72 |

| Seoul | 462.55 | 136.50 | 229.46 |

| Singapore | 664.16 | 191.29 | 152.16 |

| Bangkok | 45.73 | 23.50 | 77.7 |

| Kuala Lumpur | 84.87 | 31.70 | 64.90 |

The 53% of the IT Power capacity is phased or yet to be commissioned in Mumbai

Of the cumulative IT power capacity of 885MW built since inception in Mumbai, Live IT power constitutes23% of the overall capacity at 207.14MW. The Phased IT power constitutes 53% of the overall capacity at 470.30MW while the remaining 24% or 207.76MW is under construction.

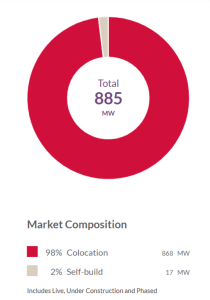

In terms of market composition, Co-location constituted majority of 98% of the IT power capacity at 868MW. The reminder was constituted by Self-build with the IT power capacity at 17MW.

Providing a deeper categorization on IT power capacity in the Mumbai market; Colocation Live Leased IT Power – 144.7MW; Colocation Live Available IT power – 45.94MW, Colocation Under construction leased IT power – 11.5MW, Colocation Under construction available IT power – 195.86MW and Colocation Phased capacity – 470.3MW.

Shishir Baijal, Chairman & Managing Director, Knight Frank India, said “The Mumbai data center market currently holds enough capacity to absorb the potentially massive data requirements that are bound to arise in a market such as India. Around 700MWof data centre capacity in this market is either under-construction or still to be commissioned. The Data Protection Bill when finalised, will be a pivotal point in the evolution of the Indian data center market and will dictate market volumes going forward.”

Adeline Liew, Data Centres Lead for Asia-Pacific, Knight Frank said: “While a new wave of COVID-19 infections may have hampered data centre development in Greater China markets this past quarter, overall, COVID-19 has actually been a boon to data centre demand in Asia-Pacific, as it has led to a tremendous increase in both appetite for the cloud due to the shift to hybrid work as well as an increase in overall internet penetration. Because of this trend, we have noted increasing interest in several markets across Asia-Pacific in both established markets as well as developing Southeast Asia markets.”

To view the latest Data Centre Report – https://app.dcbyte.com/knight-frank-data-centres-report/Q1-2022

CT Bureau

You must be logged in to post a comment Login