Trends

Smartphone ODM/IDH companies’ H1 2022 shipments declined 3% YoY

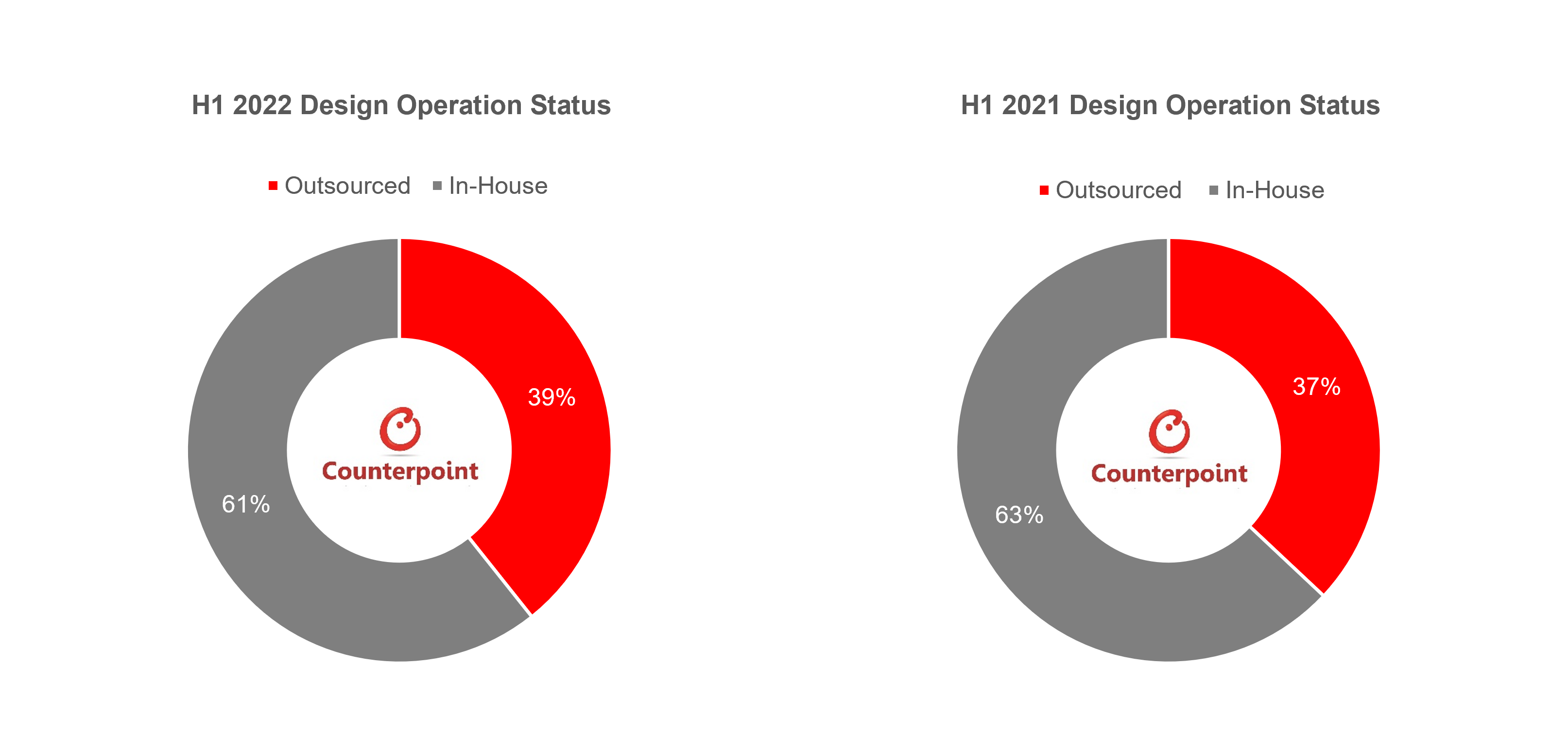

Smartphone shipments from ODM/IDH (Original Design Manufacture/ Independent Design House) companies declined 3% YoY in H1 2022, according to Counterpoint Research’s Global Smartphone ODM Tracker and Report, H1 2022. In contrast, global smartphone shipments fell even more sharply in H1 2022 due to the economic headwind, dropping 8% YoY. While the share of smartphone shipments from outsourced designs (from ODM/IDH companies) increased to 39% in H2 2022, up from 37% in H1 2021.

Senior Research Analyst Ivan Lam said, “Downtrend in ODM/IDH companies’ shipments was driven by weak performance from OPPO, and Samsung, while the increased orders from vivo, TRANSSION and HONOR contributed offset to the decrease.”

Senior Research Analyst Shenghao Bai added, “The impact of inflation, rising food and energy prices in some regions is obvious, and personal consumption has weakened, consumers will tend to choose affordable products. OEMs are also struggling with cost pressure, it is possible to allocate more mid-to-low-end products to ODMs in the future. For example, ODM shipments’ proportion in vivo rose to 20% in H1 2022, after its first ODM-made device in H2 2021.”

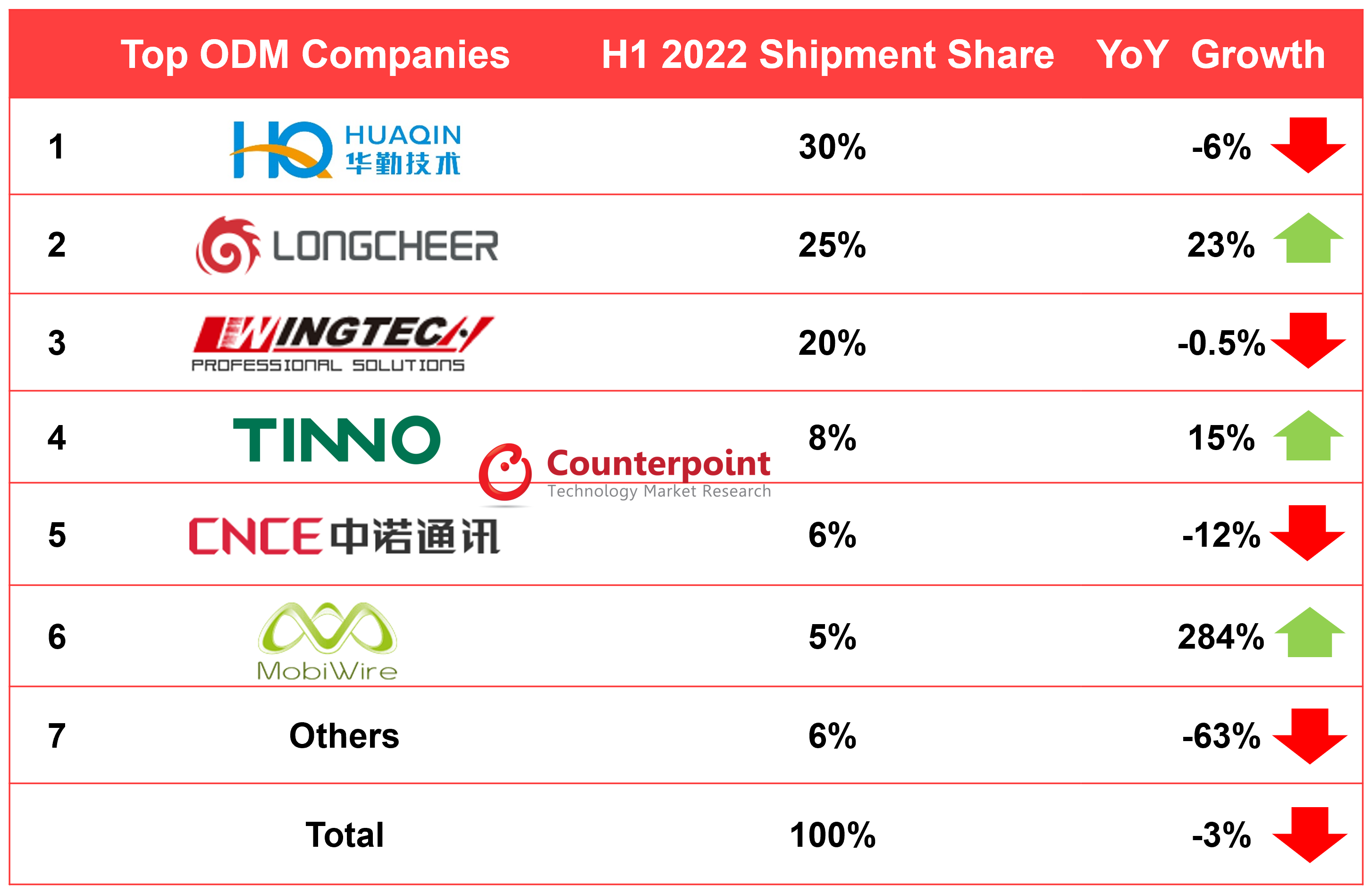

Looking at the competitive landscape of the global smartphone ODM/IDH, Huaqin, Longcheer and Wingtech continued to dominate the market. The ‘Big 3’ now account for 75% of global ODM/IDH smartphone market, increasing from 70% in H1 2021.

Commenting on the leading ODMs’ performance, Ivan said, “Affected by the performance of Xiaomi and other companies, Huaqin’s shipments declined in H1 2022 but still accounted for the largest share among ODMs. At the same time, as of the launch of this research, Huaqin is vivo’s exclusive supplier, and with the other core customers recovering in the second half of the year, it is expected to see a good increase in shipments in H2 2022. Thanks to the breakthrough of cooperating with Samsung, Longcheer’s shipments increased sharply. Wingtech’s shipments slightly dropped YoY after it shifted its focus to the semiconductor and optical module sectors. In Tier 2, Tinno’s shipments rose driven by expansion through tie-ups with more OEMs. MobiWire saw a sharp increase after bagging Transsion’s projects.”

The diversification of manufacturing in the global electronics industry has continued. While smartphone OEMs are aggressively investing in India, EMS companies such as Foxconn, Pegatron, Compal and Wistron are expanding assembly lines to India, North America and Southeast Asia.

Commenting on these trends, Ivan said, “As OEMs that lean towards in-house manufacturing, such as OPPO and vivo, may shift production to their own facilities in India and Indonesia to satisfy local requirements. Following the EMSs, ODMs are also expanding their factories into India and Southeast Asia to better support the sales of key accounts and comply with policy barriers and mitigation of tariffs. We expect the expansion to regions outside of China to accelerate after COVID-19. However, one should be wary of limiting factors such as sub-optimal supply chain ecosystem and local policy risks.”

CT Bureau

You must be logged in to post a comment Login