Trends

China Q1 2022 smartphone sales drop 14% YoY to test 2020 levels

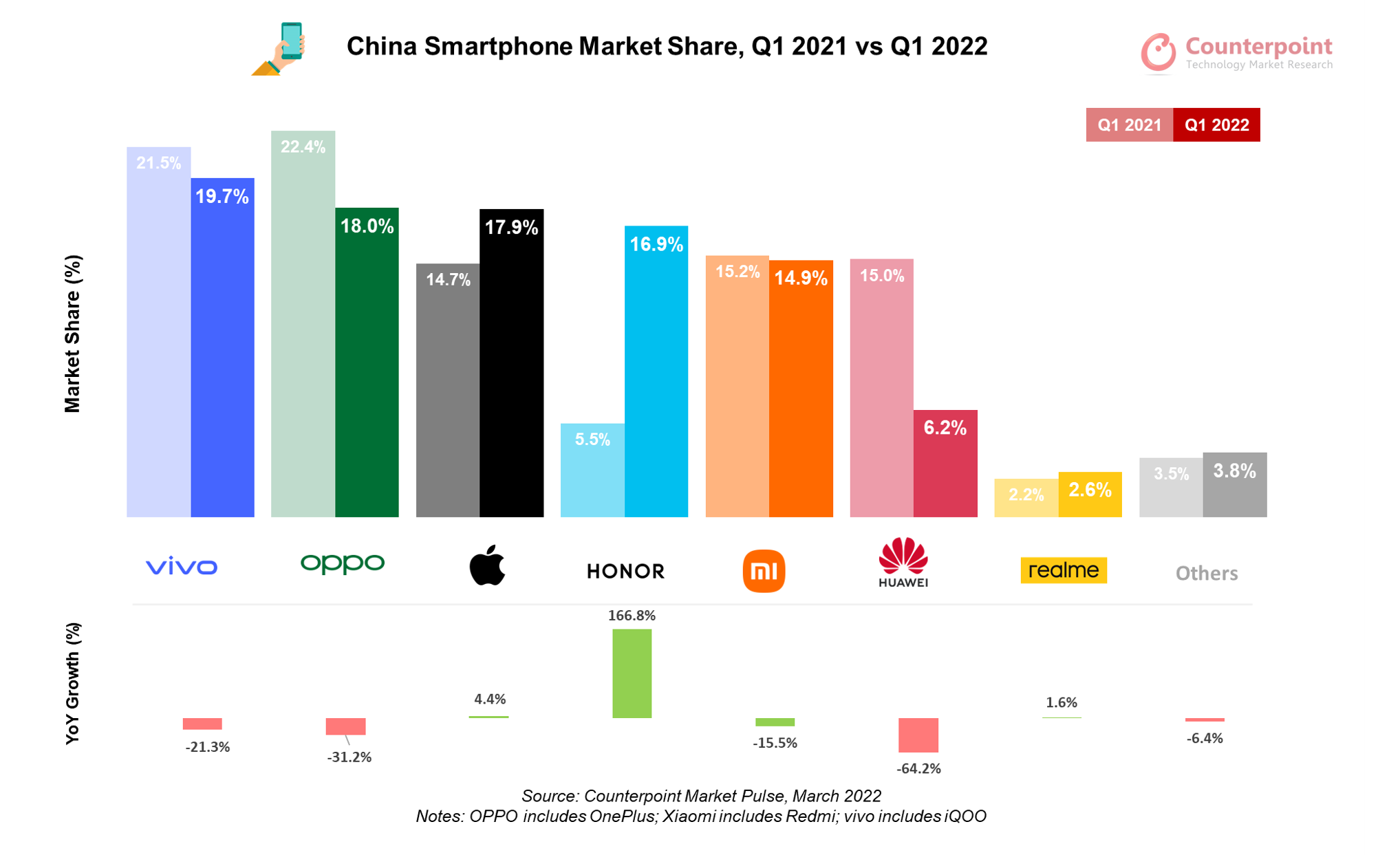

Smartphone sales in China decreased 14% YoY in Q1 2022, reaching 74.2 million units, according to Counterpoint’s latest Monthly Market Pulse report. The quarter’s volumes were close to the levels seen during the severe pandemic-hit Q1 2020.

Commenting on the Chinese smartphone market performance, Research Analyst Mengmeng Zhang said, “China’s economy grew by only 4.8% YoY in Q1 2022, lower than the 5.5% annual growth target set by the government, as the country was weighed down by the pandemic and related lockdowns. Retail growth also dropped by 3.5% in March, falling for the first time since August 2020. Unemployment rates in big cities also reached record highs. These factors, combined with the downward demand trend already visible in China’s smartphone market before the fresh pandemic wave, impacted the sector significantly.”

She added, “The smartphone market showed a declining weekly trend throughout Q1 2022, with only a small peak during the Chinese New Year holidays. We expect smartphone demand to continue to be underwhelming due to weak consumer sentiment and lack of new innovations to stimulate consumers.”

Commenting on key vendors’ performance, Senior Research Analyst Ivan Lam said, “During the quarter, vivo regained its market-leading position from Apple (in Q4 2021) with a share of 20%. The newly launched mid-end S12 series, which focuses on self-portraits and sports a lightweight and fashionable design, has received positive market feedback, especially among younger customers. vivo’s affordable Y series phones, such as the Y76s and Y31s, were also strong performers during the quarter.”

Although Apple’s sales declined from the previous quarter as momentum for the iPhone 13 series began to fade, the iPhone 13 remained the best-selling smartphone in China during the quarter. Apple has benefited hugely from Huawei’s declining sales as iPhones have become the best alternative to Huawei’s high-end devices. Huawei’s fall has prompted leading Chinese OEMs to put more resources into the high-end segment, but none of them has been able to take up a sizable share in the segment so far.

HONOR has had a strong rebound, with its market share jumping to 17% in Q1 2022 from 5% in Q1 2021. Thanks to the popularity of its HONOR 60, the brand was also the only major OEM that achieved both positive YoY and QoQ growth during the quarter, at 167% and 15%, respectively. HONOR also launched the Magic 4 series globally in Q1 2022, signaling its global ambitions.

Sales of Xiaomi devices declined YoY but outperformed the market with 12% QoQ growth in Q1 2022. Coupled with easing component shortages and strong sales performance of the flagship Redmi K40, Redmi Note 11 and entry-level Redmi-9A, Xiaomi recorded a relatively strong quarter. The launch of the Redmi 50 series and the Redmi 10A in March will further help Xiaomi solidify its position in the < $400 segment. Despite the disappointing performance in Q1 2022, the leading OEMs continued efforts to strengthen their positions in the high-end segment by launching new flagship lines with foldable models. On the new foldable smartphone segment in China, Senior Research Analyst Ethan Qi said, “Major Chinese OEMs started launching foldable devices in 2021. They view the new form factor as a way to penetrate the premium market further. During the quarter, Huawei’s clamshell-type P50 Pocket and book-type Mate X2, Samsung’s clamshell-type Z Flip 3 and OPPO’s book-type Find N were the top-sellers. However, due to foldable panel supply limitations and high price points, foldable devices accounted for only less than 1% of the market in Q1 2022.” CT Bureau

You must be logged in to post a comment Login